Updated 10-Oct-2022

Table of Contents

How I Decided

Why ETFs

Firstly a little about ETFs (exchange traded funds). These are essentially funds that bundle a large number of individual stocks, commodities and / or bonds under one fund. This allows you to easily track the trend of the whole stock market with only a handful of ETFs. This makes it easy for passive/lazy investing over longer terms. ETFs also offer low expense ratios and fewer broker commissions than buying the stocks individually. Historically since the inception of the stock market returns have averaged 9-11%. By having a well diversified range of ETFs you can also achieve these levels of returns with little effort.

Even though Irish domiciled ETFs are heavily taxed in Ireland (41% tax on both gains and dividends), I am still happy to continue investing in ETFs after weighing the pros and cons outlined in this post. This may change as I discover more tax efficient/higher performing options but this is where I’m at for now. My main reason for continuing with ETFs over pensions is that I plan to be FI at least 5 years sooner than I could access an executive pension.

Please consider the pros and cons in the previous post and do your own research before investing any sums of money. What works for me and my goals may differ largely from your own situation.

Why not one simple ETF

After reading many blog posts about portfolio options I settled with a variation to the Escape Artists suggestion explained here. Some bloggers suggest a very simple portfolio where you just chuck whatever money you have, whenever you have any extra, into one Global ETF fund like the Vanguard All-World fund (VWRL) but the reason I decided against that approach is because that fund is heavily invested in US equities (55%) and I wanted something that was a bit more diversified.

According to the Escape Artist, US equities may be overpriced at the moment which may doom long-term investors to under-performance. For example: when you buy high you need to make massive gains to make up the same returns you would have gotten if you had bought low and made smaller gains.

Why 100% stocks and no bonds

Depending on your risk tolerance you may want to put a portion (say 30% or 40% for more conservative or 90% for less conservative) of your portfolio into bonds as these have less risk and lower returns but as I have time on my side to let my investments rebound from any downfalls, I decided not to keep any of my portfolio as cash or in bonds. I’m open to the higher risk of a 100% stock portfolio which may not suit most investors.

The case for holding bonds

That said: I’ve since read an argument for holding at least 10% bonds in your portfolio and that is so that you can sell bonds at a high and buy stocks “on sale” during a downturn.

A part of investing is deciding what asset allocations you are comfortable with. Depending on how those assets perform over the year you may need to rebalance your portfolio to ensure that you maintain those allocations.

For example: You have 60% of your portfolio in an S&P 500 ETF and 40% in an emerging market ETF – during the year the emerging markets ETF out performs the S&P 500 and now your asset allocation is 50%/50%. You will need to sell some of the emerging market ETFs and purchase some more S&P 500 ETFs to rebalance back to the 60/40 split.

If you hold bonds as well as stocks, a crash may be a good time to rebalance as during a crash, money flows out of stocks (risky) and into bonds (safer), this devalues stocks and increases the value of bonds. So if you hold bonds a crash would be a good time to sell (high) and buy stocks (low) and rebalance your portfolio to your desired split. This means that once the market recovers you will own more stocks which you got “on sale” and will benefit more from the upswing in the market. If you don’t own any bonds you will simply need to wait for the market to recover (usually 2 years).

This is why it’s important to hold at least some bonds as you will be in a stronger position to benefit from market recovery than if you only held stocks.

Once I’m back to work I think I will start buying some bonds just for this purpose.

Who is this for?

As I’m currently invested in 100% stocks, this portfolio mix is probably for people very early in their investment journey who have many years of contributions ahead of them before they are able to retire.

Once you are about 5 years away from retirement you’d probably want to invest in something like 30% or 40% bonds and 60% or 70% stocks with higher yields/dividends rather than higher returns.

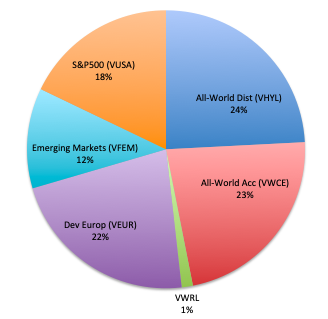

Portfolio Make-up

Below is the make-up of my current Irish ETF portfolio. All these ETFs are with the Vanguard company (See more about them below). 47% is in an all-world fund (split between distributing and accumulating), 22% in Developed Europe, 12% in Emerging Markets and 18% in the S&P 500. These funds all have varying management fees but this make-up comes to a weighted MER (annual fee) of 0.18% with an estimated weighted return of 4.10% based on each funds’ returns since inception and 2.97% in dividends. That’s excluding taxes and inflation.

And in chart form…

About Vanguard

I like Vanguard because their core purpose is “to take a stand for all investors, to treat them fairly, and to give them the best chance for investment success”, their average expense ratio is 0.10% as per 2018 assets under management. As per their website: “Vanguard is owned by its funds, which in turn are owned by their shareholders. Vanguard’s ownership structure means we have no conflicting loyalties. It’s in everyone’s interests—our clients’ and thus ours—to uphold the highest ethical standards every day. When making decisions, we are guided by a simple statement: ‘Do the right thing.'”

ETFs in Detail

Each ETF comes with a fact sheet which you can download from Vanguard’s website.

Fact sheets tell you things like:

- The fund inception date

- Total assets invested in the fund

- Exchange tickers for different stock exchanges

- Base currency (for example you may buy an ETF in EUR but the stocks base currency is USD. Your dividends will be paid our in USD and converted to EUR by the broker)

- Whether the dividends are accumulating (automatically reinvested) or distributed (paid out each quarter)

- What frequency the dividends are paid out (Monthly, Quarterly, Annually)

- Ongoing management fees

- Performance benchmarks and historical performance

- Number of stocks held within the fund

- Dividend yield (%) – the percentage that will be paid out. Usually high yield dividends have lower gains and vice versa. In your accumulation phase it’s probably preferable to have lower dividends and higher gains. Getting dividends also triggers taxable events which need to be reported and paid annually.

- Top 10 holdings (companies)

- Sector breakdown ie: what percentage of the fund is invested in Financials, Technology, Utilities, Health Care etc

- Market allocation ie: Which countries are the companies located in whose stocks make up the fund

Below are the highlights of my portfolio make-up so you can get a sense of the range of companies I’m invested in.

FTSE All-World High Dividend Yield UCITS ETF (VHYL) – 24% of portfolio

This fund is invested in over 1,500 company’s stocks. Below you can see the top 10 company’s this is invested in. The top 10 make up 13.6% of the funds assets.

All, bar 1 of my current portfolio ETFs are distributing. This fund pays dividends quarterly at a rate of 4.1%.

Here is the sector make-up.

And here is the country make-up.

FTSE All-World UCITS ETF (VWCE) – 23% of portfolio

This fund is invested in over 3,500 company’s stocks. Below you can see the top 10 companies this is invested in. The top 10 make up 15.4% of the funds assets.

Once I discovered accumulating funds I started putting any new contributions in accumulating versions. This fund pays dividends quarterly at a rate of 2.3%.

Here is the sector make-up

Here is the country make-up

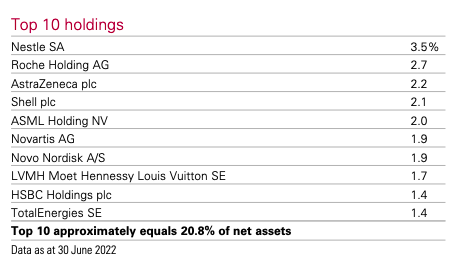

FTSE Developed Europe UCITS ETF (VEUR) – 22% of portfolio

This is a much smaller spread with investments in just over 600 companies where the top 10 listed make up 20.8% of the fund.

This fund pays dividends quarterly at a rate of 3.4%.

Here is the sector make-up.

And the market allocation.

S&P 500 UCITS ETF (VUSA) – 18% of portfolio

This one is made up of 503 companies (hence S&P 500) where the top 10 make up 28.1% of the fund.

This fund pays dividends quarterly at a rate of 1.7%.

And here are the sectors:

The market allocation is 100% US Companies which is the nature of the S&P 500.

FTSE Emerging Markets UCITS ETF (VFEM) – 12% of portfolio

This one has stocks in over 1,800 companies with the top 10 making up 22.6% of the fund.

This fund pays dividends quarterly at a rate of 3.1%.

Here is the sector make up

And the market allocation:

Performance

To give you an idea of the volatility you should expect and be prepared for, here is how this portfolio has fared so far:

Purchased: about 15,000€ worth in May 2019 + 5,000€ in Jan 2022

| Date | Portfolio impact | Loss/Gain |

| Jul 2019 | -5.3% | -780€ |

| Jan 2020 | +10.57% | +1,585€ |

| Mar 2020 | -30% | -4,500€ |

| Apr 2020 | -11% | -1,650€ |

| Feb 2021 | +13% (7.8% annualised) | +1,950€ |

| Oct 2022 | +14.82% (4.38% annualised) | +2,963€ |

As you can see, shortly after I purchased, the markets dipped. My portfolio dipped to minus 5.3% then. Even though I plan to invest for the long term, it’s very hard to stay invested when you see your money disappearing!

I stuck with it though and in January 2020 my portfolio was up by 10.57%.

Roll on COVID and at one stage I was down 30%. A month later that crawled back up to only an 11% “loss” but it was a very hard time to trust in the historical trends.

By Feb 2021 my portfolio was back up 13% overall which amounts to an annualised average return of 7.8% before tax.

Now, in October 2022, my portfolio is still up 14.82% overall but the annualised returns have almost halved since 2021 BUT my dividends have gone up from 2.32% to closer to 3%. While this doesn’t seem like much of an increase, once you have higher values invested it makes a bigger difference. For example, Right now I have about 23k in this account. 2.32% gives me 533€/year in dividends while 3% gives me 690€, a difference of 157€. If I had 100k invested it would make a difference of 678€ and if I had 1 million invested it would make a difference of 6,800€ (over 2 months of living expenses per year).

How to buy

I’ve had a few comments asking where to buy Vanguard ETFs in Ireland. You can read much more detail about how to invest and maintain investments in Ireland in this post but for a quick answer I personally use Degiro* as my online broker. Other online brokers are Interactive brokers and Trading212 if you want to check them out.

Degiro offer free commission trades on some ETFs.

Vanguard S&P 500 is one and Vanguard All World is another.

The Vanguard All World differs from the high yield world fund I am in so I must weigh up the fees and performance of these and may switch.

Here is the full list of commission-free ETFs.

You get one free trade per free share listed per calendar month.

If you are trying to copy my portfolio you don’t need to worry about timing as all the free ETFs can be purchased in the same month and the others have commission so it doesn’t matter when you buy them.

I buy the Amsterdam market ETFs as they are in Euro and not subject to currency exchange fluctuations. That said, all of my dividends except VEUR are paid out in USD and converted to EUR. This means you will still have some currency exchange exposure if you want to consideration this for your own portfolio.

Degiro have an app as well which is quite good.

As per usual, don’t invest any money you can’t live without. All investments come with risk of loss.

Updates

Based on reader feedback (thank you), I will likely be shifting this portfolio a little bit. There are ETF funds called accumulating funds which automatically reinvest any dividends into those funds.

If you don’t need the dividends right now, accumulating funds will benefit from a bigger compounding effect as you will not need to pay taxes on those dividends until the 8 year deemed disposal. Otherwise you need to pay 41% exit tax on dividends in the year you receive them even if you reinvest them.

For example I received dividends in 2019 and even though my portfolio was at a 30% loss overall at the time including the reinvested dividends I still needed to pay 300€ in tax on the dividends. That is a hard pill to swallow.

One fund I will likely be switching is the All World High Dividend (VHYL). I will be switching to VWCE which is the closest equivalent accumulating fund with lower fees. The fees are 0.22% instead of 0.29% and higher 5 year returns 6.65% instead of 6.35%, full fact sheet here. That said it’s a much higher price point (79€ per share instead of 49€) so my position will be weaker. I’ll also need to pay taxes on my gains by swapping so need to take all that into consideration.

Another reader kindly researched the other accumulating fund equivalents. I had a look at the fact sheets and they are exactly the same with the exception that one pays out dividends and the other doesn’t. Same stocks, same companies, same allocation, same fees etc.

Here is how they map out:

| Distributing | Accumulating | |

| Vanguard All-World (VWRL) | = | VWCE |

| Vanguard Developed Europe (VEUR) | = | VWCG |

| Vanguard S&P 500 (VUSA) | = | VUAA |

| Vanguard Emerging Markets (VFEM) | = | VFEA |

Here is some more information on fund examples with accumulating vs distributing ETFs if you want to read further.

Free ETF Comparison

Yet another reader pointed out that the trading platform Trading212 has VWCE as a commission free ETF. I don’t know much about that platform and haven’t figured out if there are any downsides to having funds in different platforms.

Only thing I can think of off the top of my head is it might make it harder to balance your portfolio if you need to extract money from one and move it to the other. Also harder for you to see overall losses or gains and possibly harder to compile gains for deemed disposals and other tax reporting etc.

So in terms of free ETFs in my current portfolio VWRL and VUSA are free in Degiro, VWCE is free in Trading212 but Trading212 does not seem to have the other accumulating ETFs listed above available to purchase. None of the accumulating funds I’ve listed are free in Degiro as it stands. These are recently created funds so that’s not to say Degiro won’t add some eventually.

I still think I will switch from distributing to accumulating even though they aren’t free to purchase as the money I’ll make in compounding by not having to pay taxes on dividends until year 8 will outweigh the cost of buying them once a month or once every 2 months.

Would love to hear your feedback or if you have anything else to add that other’s might benefit from do let me know and I’ll update the post.

Although this was one of the simplest posts to put together compared to some of my more extensive articles, this one seems to be one of the most popular so the more I can add that would be of use, the better for the wider audience.

* This post contains referral link where I get a bonus if you sign up at no cost to you. All investment carries a risk of loss. Do not invest any money you can’t afford to lose.

Spreadsheet templates

Want access to Mrs. Money Hacker’s spreadsheet templates?

I launched a member’s area where you can gain access to all the latest spreadsheets which have taken hundreds of hours to create and fine-tune over the last number of years.

Check out this page for more details and a sneak peek of what you’ll get if you sign up.

The Irish UCITS do not suffer any DWT at source.

Any ETF with IE in the ISIN.

Are any of your Vanguard such ETFs?

Do you get taxed any DWT at source?

I have a German ETF with ishares, and it gets 20% taken at source by my Irish broker. Its a minefield, the different tax treatments.

HI there, Yes all of my Vanguard ETFs are Irish domiciled UCITS and as far as I can see have not had any withholding taxes applied at source. I believe that other Europeans purchasing Irish domiciled ETFs are also charged something like 30% withholding tac which they cannot claim back so that’s at least something to be thankful for. Would it be worthwhile for you to sell your German ETFs and purchase Irish ones to reduce your taxes withheld? Unless you can claim back toe 20% from the German shares? Just more paperwork which is annoying!

Would it not make more sense to buy US or Canadian domiciled ETFs and simply pay 30% CGT rather than 41% at the higher rate of Income tax?

It would indeed, however back in 2018, new regulations (PRIIP regime requiring all funds to come with a Key Investment Document (KID)) came in that stopped retail investors from being able to buy US or Canadian-domiciled ETFs. This has not changed as far as I know.

Are you using the dividends earnings for income? If not, wouldn’t it make more sense to buy the accumulation equivalents of your ETFs. That way you gain up to 8 years (deemed disposal limit) of tax free earnings and avoid brokerage fees when reinvesting the dividends.

Hi there, no I’m not using the dividends for income just yet. And yes it would make more sense to use accumulating ETFs! I only recently heard of them so haven’t re-configured my portfolio. Do you have a list of similar ETFs which would be accumulating? Or is there some indicator in the name? Rather than digging through fact sheets?

https://www.bogleheads.org/wiki/EU_investing

There’s sample accumulating and distributing portfolios on there. Might also be with reading the investing from Ireland page on there.

Hi Meagan. I have a question on the 8 year deemed disposal on ETFs. I’ve just set up a Degiro account and am looking to invest for a long period (over 15 years) using euro cost averaging. But on the 8th anniversary there is a declaration that needs to be made to Revenue. Will this affect the compounding potential?

Does the 41% tax on gains come from the fund itself or can I make a separate payment to Revenue which will mean that my ETF is not touched? Apologies for my lack of knowledge. I really am a novice at this.

Thank you

PS. This is an accumulating ETF.

Hi Mike, Yes, unfortunately, the 8 year deemed disposal does impact compounding. As far as I know, you can pay the deemed disposals from either within the fund or outside the fund but as you get more and more gains the taxes will become quite hefty. Say you have 450,000€ invested and the gains are 32,000€ for the year, your exit taxes 8 years later will be 13,000€. That’s a fair chunk of change to have kept aside. The deemed disposals apply to both distributing and accumulating funds. The only difference is that the exit tax would need to be paid on dividends for distributing funds in Year 1 as opposed to only needing to pay them in year 8 on both dividends and gains with accumulating funds. This means that the dividends can compound without incurring taxes for 8 years resulting in better portfolio growth.

Hi Meagan,

This was also my plan. Just wondering if this means you could potentially have to sell ETFs to pay a tax bill?

Hi Kirsten, yes if you don’t have the money to hand, you may need to sell your ETFs to pay the tax bill, which could result in taking a loss that you can’t carry forward unfortunately.

Is it possible to purchase the VWRA ETF on the Amsterdam exchange or other euro exchanges? On degiro it is listed under LSE. ISIN is IE00BK5BQT80 I think. Is this the same one you invested in?

Hi Ronan, Just had a look there at the fact sheet and you are right to question it. VWRA is the USD ticker. The EUR ticker for the same fund is VWCE. I haven’t invested in it yet myself so hadn’t gotten that far. I’ll update the post. Thanks for pointing it out.

Hi Meagan, I’ll check out VWCE. Thank you for the clarification and the speedy reply.

Just a heads up, Trading 212 has VWCE commission free.

Cool I’ll check that out and update the blog post next chance I get. Thanks

Hi Meagan,

Good info on ETFs.

Do you know if the 8 year deemed disposal 41% tax applies to traditional Vanguard index funds (non ETFs).

Say the Vanguard U.S. 500 Stock Index Fund (Bloomberg:VANUIEN) which is also domiciled in Ireland?

Hi Jonathan, That’s a great question. I hadn’t come across that yet so unfortunately I don’t know the answer. I do know that Revenue are very helpful if you give them a buzz. If you get to it before I do, please let me know what you find out!

Hi Meagan,

How does the 41% tax affect the SWR of 4%. From what I can gather if an ETF returns 10% (which I feel is optimistic) and inflation is 3% then the real rate of return is more like 4.65% after fees. (I may be wrong) Do you think does the 4% rule still hold up in this case? Cheers

HI Daire,

Here is an excellent article in terms of historical returns since 1926 (the history of the stock market), showing different returns for various allocation splits https://www.financialsamurai.com/historical-returns-of-different-stock-bond-portfolio-weightings/.

In terms of planning all we can do is base it on historical data. A 100% stock allocation historically has returned 10.2%. Of course, if you want to be cautious you can build in a buffer in your analysis :).

Historical inflation in Ireland for the last 30 years has been 1.9%, though if the value of your portfolio is based on US companies, maybe you need to apply their inflation rate, I’m not sure.

Anyway to your main question: I did some analysis looking at a 20-year accumulation and 30-year withdrawal using the 41% exit tax and a safe withdrawal rate of 3.5% seemed to be more cautious. This means you need 28 times your annual retirement income instead of 25. For me, I plan to continue earning money in “retirement” so I’m happy to use 25 times in my calculations but if you want to officially retire on an ETF portfolio then 28 times is probably a better figure to aim for.

Hi Jonathan – did you ever find an answer on this? Thanks

Thanks for the speedy reply. I was just going larger on the inflation rate after reading ‘how to own the world’. A section of that book explains how ‘real inflation’ is much higher than the official numbers. I’m not trying to poke holes in your plan, I’m just trying to figure out my own plan. I’d love to invest in ETFs but I feel a PRSA with standard life invested in a vanguard global stock fund is the better option in my circumstances. I think it would take me until age 60 to save enough in an ETF to retire anyway. I love your blog, it’s really well written and helpful. Thank you

Hey! Sorry if I seemed defensive lol, not at all, glad to have the questions as I’m not always right! Also, of course, you do what works for you. If it will take you time to build your retirement pot then pensions definitely make sense. Just be sure to check the fees and performance to make sure your money is always working for you as best as possible. Glad you’re liking the blog 🙂 It’s great to hear from readers.

Hi Meagan,

Im reconsidering my allocation to pension v taxable and was wondering would you have any idea what the tax treatment of an ETF held with Degiro is once you start taking it as income? Would the exit tax still be due as well as income tax, prsi and usc? Thank you.

Hi Daire, My understanding is that the 41% exit tax on gains and dividends is all that’s due on withdrawal or as deemed disposal every 8th anniversary (as you’ll already have paid income tax+PRSI+USC on the initial contribution), so in a way the silver lining of the deemed disposal is that you pay the taxes due along the way so that when you withdraw you just file and claim back the credit for taxes already paid on every 8th anniversary.

Hi there, I just had a possibly silly question…I’m new to investing. When you make your tax returns for your irish domiciled accumulating etf investments, is it just the form 12 you need to fill out each year if you sell your investments/8-year gross roll up period ends, or do you need to file anything to let revenue know you’ve bought an etf even though you plan on holding it for a number of years. I’m planning on investing each month and was wondering how tedious the returns would be.

Not a silly question at all. I haven’t got a clear answer on this yet myself as I’m due to file my first return this year. Once I figure it out I’ll update the blog. I know with employee share purchase programs you need to file tax when you buy shares as well as when you sell but I’m not sure if something similar applies to accumulating ETFs. In terms of figuring out the returns I think it’s simple enough in that Degiro (or whichever broker) provide you with a summary of your gains and dividends for the year for tax purposes. You then use these figures for figuring out your taxes due.

Revenue are very good to provide guidance on these things if you get a chance to ring them before I do, let me know 🙂

Hi Meagan,

Thanks for the blog, I’m a newbie too and learning about the Irish taxes on my investments too (I use Trading 212 and want to add Degiro too as brokers). I want to be a dividend investor to eventually live on dividends when I’m middle aged. I am just a bit confused with this whole 8 year thing. I am 23 now and I am not planning to sell for the next 25-30 years while continually adding to my accounts, but from my understanding, I will have to pay the deemed disposal income tax every 8 years on the total gains of the account? or is it the case that I pay for the gains of yeas 1-8, then 9-16 etc.? or do I withdraw my funds, pay the taxes then invest again? or after year 8 I start to pay annually? I’m just confused???

Thanks,

Mamobo

Hi Mamobo, Thanks for reaching out. As far as I understand the deemed disposal for the gains you made in year 1 are paid in year 8, the gains you made in year 2 are paid in year 9 etc. You can pay for these taxes however you like, either from funds inside the investments which you sell off OR from funds outside the investments. Then when you actually sell you’re the taxes paid as a credit against what is actually owed on the actual gains or losses you made. I’m not 100% on this but will do a post on it once I have confirmed. You can also ring Revenue for clarifications like this, they are very helpful, I just haven’t gotten around to it yet myself!

Hi Meagan,

Thank you for this helpful blog!

I am currently living in Ireland and thinking about starting to invest in ETFs. However, I intend in moving to a different EU country in less than 8 years. I was wondering if you have any idea whether by changing domicile do I still have to pay the 41% tax when changing countries, since it would be an EU country and the taxation rules from that moment on would be that country’s ones.

Hi Marta, Thanks 🙂 If you were not born in Ireland and do not intend to live long-term in Ireland then you are not Irish domiciled for tax purposes now or in the future. Even if you are resident for tax purposes you are not Irish domiciled. If you live here for 3 years or more you are considered ordinarily resident and when you leave you will still be liable for taxes on Irish sourced income on your worldwide income for 3 additional years. ETFs are not considered Irish sourced income though so I think that you will only need to pay tax in your new countries rates. You will not have the 8 year deemed disposal either but will need to register with Revenue or your broker to prove that this is the case. You will need to check the double taxation treaty between Ireland and your future country to see what taxes will be liable at that time. You may also have withholding taxes applied by your new country so be sure and do your homework in advance of such a strategy. There is an Irish company that specialises in cross border taxation guidance called etsi.ie if you want to reach out to them. I also detailed a bit more around this concept in this post https://mrsmoneyhacker.com/tax-loopholes-for-irish-investors/ – edited to say I am not a qualified tax advisor so do not take what I say here as gospel, please validate my understanding is correct with a specialist.

Thank you very much for your quick and clarifying reply!

I was reading your other post about this concept and I figured I could go by the strategy you used with Canada too. If the investment and taxation is done in my home country it could be more profitable from the tax rates point of view, as long as the money is not remitted to Ireland and I wouldn’t have to change. I will inform myself better about this matter but you’ve given me a good view to start with!

Keep up with the good work!

Thanks for the list of ETFs. I hope you will be keeping it updated?

Do you know any brokerages that will open an account for Indian residents? I am aware of only IB as an option which is unfortunately not the most suitable for smaller passive investors.

Thank you.

Hi there, yes I will be keeping the list up to date as I continue to invest now that I am back to work. Unfortunately, I don’t know of any brokerages for Indian residents though you may be able to post your question or find your answer in the bogleheads forum where others discuss the specifics for investing in India and other countries. https://www.bogleheads.org/forum/viewtopic.php?t=298291

Hi Meagan,

Thanks for in info above it’s really useful 🙂 Just on the VUAA fund, I agree the benefits of accumulating the dividends versus the distribution however the only VUAA fund I can find to purchase in Ireland is on De Giro.

My main concern is the fund is in US Dollars, so after 8 years there is the risk of currency fluctuations and it could take a massive chunk from the final amount available after tax etc.

Do you know of any brokers that sell a Euro version of VUAA?

Thanks

Hi there, No, unfortunately, I haven’t found a Euro-based fund. As the S&P 500 is an index of the largest US companies, the underlying funds will be in US dollars and so even if you could find a Euro-based fund the currency fluctuation risk would still be a factor at least during accumulation, though I get the issue on withdrawal many years later if you had just converted the currency on purchase. Even still though the value of the index will follow the US dollar so even if you had bought in Euro I’m not sure you would be completely shielded from the link the US dollar anyway – I’m not sure, that’s my logic anyway 🙂

When I started out I was also researching the currency aspect of the ETF’s and everything I read said I should not worry about it. The papers/blog posts i read all indicated that after you factor in the extra costs a fund would have (higher MER) to charge to do it, the risk of the hedges themselves gaining/losing value etc. that at best you might be slightly (<0.5%) better off in the long run. I settled on a portfolio of AGGH as my bond ETF which is EUR hedged and accumulating as it was available and then VWCE as the accumulating equity ETF which is USD based.

Hi – Thanks for sharing all the details. I am currently looking where is best to invest and you page has been very useful. I had a few questions – Are mutual funds liable to exit tax and the higher 41% tax rate or do they fall under cgt rules and only taxable on disposal? Why do you invest in EFTs over mutual funds? Why do you invest in UCITS EFTs and pay 41% tax vs US domiciled EFTs and pay cgt? Thanks so much for your help

Hi Paul, I’ve actually done very little research into mutual funds, when I read about them in Canada it seemed the FI bloggers avoided them due to high purchase costs, high ongoing costs and costs on sale and also the lack of control on what they are invested in ( very similar to my main bugbear with pensions). I did a quick search about them in Ireland and I could only find very outdated articles (one from 1999 and one from 2012!) – maybe they are not available in Ireland? The article from 1999 seemed to say that taxes were taken out from the fund at 24% and no CGT or income tax applied thereafter, but that was before exit tax was even a thing so wouldn’t rely on that information too much. If you do find anything up to date on mutual funds in Ireland do let me know!

Also re: US ETFs, you can no longer buy those as a retail investor in Ireland – you could access them through a managed broker but then you are paying management fees which I like to avoid.

Thanks Meagan. I tried doing some research here. From what I can see, you still get hit with the 41% tax by investing in mutual funds, but I think you are able to offset gains and losses which you wouldnt be able to do if you have multiple ETFs. Found some good funds on Vanguard until later finding out that you cant invest in them in Ireland 🙁 So now thinking an ETF might be the way to go unless I can find a low fee broker for a mutual fund – but seems limiting the number of ETFs invested in might be best so dont have losses that cant carry forward / offset. Have you retained much in ETFs or focused mostly on clearing your mortgage? I also have a chunk of mortgage to clear, so could be another viable option. Thanks again

Hi Paul, apologies for the LONG delay. Ya I am focusing on clearing our mortgage first before continuing to invest in ETFs, only a small portion of our net worth is in ETFs for the moment but once the mortgage is cleared that will be our main investment vehicle to work towards passively covering our remaining expenses.

Im living in ireland and have started buying stocks , really want to start investing in eft’s i tryed to join the vanguard platform but cant because im irish is there other platforms in can join i know there is other eft’s that mimic the american ones any idea where i can find these ???

Hi Stephen, Apologies for the LONG delay! I use Degiro to buy my ETFs, you can find the full list of ETFs on offer on there and then google the fact sheet for the funds you are interested in to see the makeup. JustETF.com is also a great website for finding ETFs you’d like to invest in.

Hi Megan,

I’m new to all this but wondering why you chose investing in ETFs instead of Investment trusts? As investment trusts are taxed at 33 CGT and not 41 marginal rate, they also do not have forced deemed disposal every 8 years.

Thanks

Hi Mark, Good question. I have started dabbling in investment trusts due to the reasons you outlined, however, investment trusts are riskier and less diversified than ETFs. Investment trusts, as far as I know, are investing in a single company to buy stocks on your behalf rather than buying the stocks themselves through an index. So if anything happens to the company that is holding the investment trust, you could lose your assets. The rule of thumb I am trying to follow is not to have any more than 5% of my portfolio in any one investment trust. They also have higher purchase costs than ETFs which can add up over time.

Hi Mehan,

Many thanks for you reply.

Just as an example, ALLIANZ TECHNOLOGY TRUST PLC , has an annual fee of 0.80% and OCF .88%, so this is slightly higher than say .25 (roughly) for EFTs. But wouldn’t CGT more than makeup for this?

I’m completely with you on the ‘eggs in all one basket’ re it being PLC on the stock exchange, but I’ve read that these managed funds outperform EFTs in general?

I actually know nothing about any of this, but would love your thoughts. Oh yea,

last thing, any thing any thoughts on P2P lending, such as Mintor, or Peaberry?

Thanks!

Hiya, Just ran a simulation for my own curiosity and as with all my other comparisons, it’s much of a muchness. I might do a post on it for the level of detail but at a high level: Investment trusts and stocks are subject to stamp duty. IT’s are in GBX (British pence) and therefore subject to 0.5% stamp duty on each purchase on top of Degiro’s purchase costs which are a combination of flat fee per transaction and a percentage of the purchase as well. In my simulation the IT portfolio was 14.5% better off after 20 years BUT that does not account for currency exchange risk and fluctuations. Looking at the last 5 years alone, the range between EUR and GBP has swung as much as 21% between high’s and low’s. So while the IT portfolio MIGHT be 14.5% better, it could also be 21% lower at any one point due to currency fluctuations. Ultimately, I’m looking to keep my portfolio simple with little risk and little reliance on how another country’s economy is doing (in terms of currency value). In terms of P2P, not my cup of tea, too high risk given the lack of regulation and the number of companies that recently went bust and there’s a somewhat moral element for me as well considering the people taking the loans are usually people who can’t get loans anywhere else and are paying ridiculous rates for things they probably don’t need. Feels a bit like taking advantage of people in poor financial state, when the whole purpose of my blog is to help people financially – bit hypocritical.

Hi,

Would it be possible for you to detail the exact ETF you invested in that accumulate. When reviewing within degiro there are two or three of each with either MIL or XET from a European perspective. I am trying to ensure I buy the correct ones that will accumulate.

Thanks

Hiya, I haven’t actually switched to the accumulating ETFs yet but you can find if it is accumulating or distributing in the fact sheet for each. Just google the index and fact sheet. Here is an example of the fact sheet for VWCE and under dividends, it says accumulating https://global.vanguard.com/portal/site/loadPDF?country=pt&docId=31355

Hi,

Thanks for the quick response I think I’ll be going with the VWCE and VUAA on a monthly basis. Going with the ones XET as I believe this is just the location of where the trading is based out of. Reading the documents attached in degiro both state accumulating.

Sounds like a plan 🙂 Ya the exchange is just where it’s traded. My understanding of the difference is just that it’s a different market ie: think of it as a shop, one market is selling the same thing as another – when you want to sell your own shares/ETFs you want there to be people willing to buy from that shop. If you try to sell from a shop that doesn’t have as many buyers you may not be able to sell your ETF’s as quickly as another market. In terms of demand I don’t see any major difference between the European markets so shouldn’t be a concern.

Hi Meagan,

Just a question on the accumulated etf’s that reinvest the dividents back into the fund. do you know what dividents they do pay back into the fund. just trying to work out the effects of it on the compounding of the fund.

Regards

Hiya, the dividend yield will be in the fact sheet for each. In this fact sheet for VWCE for example on page 3, it shows the dividend yield is 2% https://global.vanguard.com/portal/site/loadPDF?country=pt&docId=31355. As for the performance quoted in the fact sheet, it includes the assumption that all dividends and capital gains are reinvested so this is already taken into account in the performance rates quoted. Some fact sheets do not include this method so it’s important to read the fine print on each to determine how to model the growth in any analysis.

Great read, i am in investor from Germany, can you emphasis on expense ratio in long run, as i see some etf of vanguard example VFEM has 0.22%, is it the same in ireland too, if so, does it matter to you? Or you have set some limit yourself when choosing it.

Hi Mary, Thanks for reading. In choosing my allocation the fees only made up a part of the equation. I looked at them as a whole like, market exposure (all US, emerging markets, developed europe), as well as the expense ratios and historical performance. I played around with my allocations to reach a happy medium between all of these elements. For VFEM for example, the risk and volatility is higher but so too were the returns at the time. As this is a long game for me I was happy to take the higher fees for the riskier higher returns. I don’t have a maximum, as long as the fees are justified by higher potential returns for example. I hope that makes sense?

Have you considered holding your ETF’s in a PRSA account instead of DeGiro?

Irish domiciled ETF’s are exempt from the “Deemed Disposal” rule if the units held are assets of a PRSA and the PRSA administrator (e.g. Davy in Ireland) has made a standard-form declaration prior to the chargeable event taking place i.e. prior to the 8th anniversary of ETF being purchased.

The obvious drawbacks, though, are the PRSA admin fees and the fact that the PRSA can’t normally be accessed until you’re 60.

Hi Darragh, thanks for the comment. Yes I have looked at a PRSA and executive pension as part of my strategy and although it gets me to my FI number faster, the fact that I can’t access it for many years outweighs all the other benefits in my situation. I hope that we will be in a position to reach FIRE by my mid 40’s at the latest so even if I split between PRSA and after-tax investments, it will complicate my withdrawal strategy and I’m opting more and more for the keep it simple approach. For anyone not planning to reach FI until 60, then PRSA is a no-brainer as long as you can keep the real rate of return at around 6% after fees and inflation.

Hi Megan,

very interesting article!

Did you also backtest your portfolio?

This website seems great for playing around and adjust portfolio according to past performance: https://backtest.curvo.eu/

I wonder if you would make any adjustements looking at the results?

Hi Meegan

With regard to investing in UK trustfunds versus ETF.

While UK trusts will usually all have higher ongoing charges vs, ETF, you will benefit from lower capital gaines tax, including the annual cgt allowance of 1270euro, if you capture some realised gain each year, but this may or may not be worth the effort once investment gets larger.

Most UK trusts are actively managed rather than passive, and some investors prefer passive index tracking ETFs because they closely follow an index and have low fees.

And lastly their is less choice with UK trustfunds compared to ETFs, but even with all these factors, I believe they can be a good option.

You raise the issue of currency exposure to GBP because the trustfund is in GBX, but if you invest in a trustfund, that itself buys a basket of shares, your true exposure should be to the currency of the underlying investments, which I think is explained in this post (which is talking about ETFs but same logic should apply to Trustfunds)

https://andrewhallam.com/expatriate-investors-does-it-matter-which-currency-your-etf-is-listed-in/

Do UK investment trusts perform better than ETFs, I guess that depends on which ones you pick. There are some very high performing funds in 2020, which are focussed on US market with high exposure to US tech, but I am sure it is possible to select a number of uk trustfunds to cover your desired geographic regions, equity or bonds.

Hi Andrew, Thanks for that. I agree with all you have said. At the end of the day, it comes down to personal preference in terms of effort to maintain, risk and goals. Some will be chasing the highest net worth while others are happy to balance off the maintenance, effort and risk against potential lower returns in the long run.

Hi Meagan,

Having serious troubles trying to pay for gains on ETFs for 2020. I am a PAYE earner and revenue have informed me that I pay using MyAccount and not ROS. I have multiple “my enquires” on it and multiple telephone conversations with Revenue. The latest advice from Revenue was to utilise MyAccount as I am a PAYE worker. However there is no section to enter ETF gains? The Revenue told me I could post in Form12 and write a note on it with ETFs? Surely there is a better way. I have talked to at least 5 different Revenue phone operators. Thanks

Hi Joe, Thanks for reaching out. That sounds pretty frustrating alright. Personally what I have found with filing my own taxes over the years is to just make my best effort and file SOMETHING and pay what I think is due. If it’s not the right form or not the exact calculations it’s for revenue to tell me otherwise. As long as you are filing and paying something if something is due, then they can’t apply penalties, only interest on the amounts not paid (if you didn’t get the amount right). As exit tax is fairly straight forward, I’d just file the form 12 as you have been advised by the latest person and submit the payment. Judging by this article, form 12 does look like the right form for someone whose main income is PAYE and whose income from other sources does not exceed 50k https://irishaccounts.ie/blog/2011/03/income-tax-form-11-self-employed-v-form-12-not-self-employed/. Looking through this form 12, check out the dividends and capital gains sections for where your ETFs best fit and as they say add a note that they are ETFs https://www.revenue.ie/en/self-assessment-and-self-employment/documents/form12-2019.pdf Best of luck with it.

Hi Meagan,

Great article! Have you considered purchasing ETF’s through a USA broker?

Some advantages (as I understand but could be corrected):

1 – You can offset losses from one ETF with gains from another.

2 – You do not have to do this 8 year ‘deemed disposal’.

3 – Capital Gains are treated as CGT (33%) (Dividends as Income tax)

4 – Loses can be carried forward

5 – You can avail of the CGT allowance of €1,270 per year before you have to pay CGT. Of if you open a joint account you can earn €2,540 per year tax free.

Hi Brian. We can’t directly purchase US ETF’s as EU citizens as they are not meeting the EU regulations, no KIID etc. There is a loophole where we are still able to trade in the options of the underlying US ETF unit shares, and if assigned shares this way you will receive them into your EU brokerage account and ar free to sell them form there. With options contracts sized at 100 units/contract, it’s a possible route but more complex and larger volume trades each time.

I actually found a recent analysis that proves what I had suspected, which is EU accumulating ETF’s are not actually as bad as they might sound in reality. Because the US ETF’s are required to pay out dividends, and you are then taxed on that every payment at your marginal income tax rate it actually only takes the market dividend rate to head towards 3-4% to actually tip the equation in favour of holding EU accumulating ETF’s where the dividend compounds tax-free for 8 years. Now, the current dividend rate is a little shy of about 2% currently I think, so US ETF’s will still edge it out vs. EU accumulating ETF’s at the moment, but not be nearly as much as some may think.

See: https://anirishinvestorsguide.com/2018/10/27/taxation-of-etfs-in-ireland/

Hi Paul,

Some US brokers allow the purchase of US ETF’s for Irish people. I had to switch US brokers to avail of this. When I asked my existing broker why they did not allow it when another US broker does they said that different brokers interpret the standard differently.

Regarding the options, yes I am aware of that ‘loop hole’ but an expensive one to utilise as you mentioned.

That link was very good – thanks for sharing Paul!

Do you know if this deemed disposal is still applicable if you purchase an EU ETF through a Irish pension fund?

Hi Brian. Yes, I have seen a couple of US brokers who allow it, and some that did for a while are now closing it down so I don’t think it will last forever as a long-term option. I think the trigger to enforce it might be if they open a EU entity and have to get regulated here.

On purchasing in a pension, I don’t have personal experience of it but I believe there is no deemed disposal/exit tax to worry about in that situation as the pension is allowed to grow tax free.

Thanks Paul.

Hi Brian, Thanks for the feedback. I agree with what Paul added. Also I did look at all kinds of options as I have access to Canadian investment accounts. Ultimately I decided to keep it simple and try not to obsess over the absolute best tax treatment and so on. The effort required to transfer the money to Canada (incurring exchange fees and added currency fluctuation risk), on top of complicated withdrawal strategy and having to file Canadian taxes on top of Irish each year and so forth, all for shaving off MAYBE 6 months from my time to financial independence, in the end wasn’t worth the effort to me. Now I’m just trying to stick to my path and trust that with each investment I am stepping towards more and more financial freedom.

Hi Megan,

Yes, I can understand the ‘Keep it Simple’ approach!

Thanks.

Hi Megan,

You mentioned that “the reason I decided against that approach is because that fund is heavily invested in US equities (55%) and I wanted something that was a bit more diversified.” Can you help me understand why you invested separately in the S&P 500 as I thought that this would only increase your exposure (risk) to US stocks even further? The top 10 companies are almost identical to the world ETF. Maybe I misunderstood you?

Thanks.

Hi Brian, Ya the S&P500 is 100% US. My point was that I didn’t want to JUST invest in the All World fund as it was 55% US exposure. By buying 2 other ETFs that have NO US stocks in them, my US exposure is down to about 34% overall including the 16% I have in the S&P500. Does that makes sense? I see what you’re saying that why didn’t I just omit the S&P500 and invest more in the All world. I suppose I like the S&P500 ETF because it’s a lower annual fee of 0.07% instead of 0.29% that the all world has. It also has better historical returns and lower dividends (which usually indicates higher growth potential).

Understood. Thanks for clarifying.

Does anyone know much about the tax for non eu or US residents. I live in a tax free country, so I use ETFs domiciled in Ireland, then only pay the 20 percent withholding tax. As far as I know, there are no other tax applicable for me. Had I bought us domiciled ones, I would have to pay capital gains etc.

Does anyone know how the 20 percent tax is paid?

I got my first dividends but I didn’t see any tax taken off.

Hi Mike, As far as I know your online broker will disclose and summarise any withholding taxes on your annual tax report, you may not see it on your dividend payout. Log into your online broker and see if there are any annual tax reports in your documents section. In there it should detail any taxes withheld at source. As far as I know withholding taxes are withheld at source by your broker and you can claim them back when you file your taxes at the end of the year if you are eligible to claim them back.

Hi! This is very useful.

I’m just wondering if you have a recommendation for an Asian markets ETF such as iShares MSCI All Country Asia ex Japan ETF, AAXJ. I can’t seem to find a similar one on Degiro.

Thanks.

Hi there, check out VFEA (emerging markets), it’s got very similar underlying funds to AAXJ.

Thank you! I seemed to have missed that one 🙂

It’s a minefield when it comes to etf and dividend tax. In ireland do I just have to pay 25% dividend tax to revenue as income tax? Am I missing any other tax? Thanks

If you are investing in ETFs they are subject to something called exit tax which is currently at 41%. ETFs also currently have an 8 year deemed disposal where you pay taxes on the 8th anniversary of each purchase. On the other hand, stocks and investment trusts are subject to income tax rates for dividends and capital gains tax for gains. Definitely, a lot to consider but for me the simplicity of ETF investing keeps outweighing all the other investment options even if I will pay more tax in the long run.

Thanks Meagan, every cloud I guess.

Hi Meagan, Just had a question about taxation in relation to ETFs. I understand that if you hold an accumulating Irish domiciled ETF, tax is only due on exit or every 8 years. Does this mean that annual Form 11 tax declarations are not required for an accumulating Irish domiciled ETF, unless you are selling or at the 8 years of deemed disposal?

HI Prateesh, Unfortunately, I don’t have a clear answer on this. If you look at the form 11 there is a place to inform them of your acquisitions/purchases of stocks as well as a place to input purchases of offshore ETFs but no specific place for Irish domiciled ETFs. Revenue themselves I think are still figuring this out so it’s hard to get a clear answer. I have heard of Revenue telling people to calculate their taxes due, make the payment and write them a note telling them what it’s for as there is no clear place to enter it on the current tax forms – so it’s all a bit up in the air. The best steer I could give is to call Revenue directly and ask them to make sure you are covered and compliant.