This post will go through my take on how the pandemic market volatility and uncertainty has changed my investment strategy and financial freedom plan.

Firstly, before I get into a financial post, I want to acknowledge that people are losing their lives. Front line workers are exposing themselves every day to help fight this pandemic. Our lives are impacted psychologically and emotionally with social distancing and isolation. With balancing childcare with full-time jobs. For those of us lucky to have kept our jobs.

Thank you to everyone who is doing their part!

And now onto a far less important read about how my financial situation has been impacted.

Table of Contents

Emergency fund

First and foremost this situation has been an eye opener to my emergency fund approach.

Current approach

When I went on maternity leave I had about a year’s worth of living expenses in savings. Almost a year into my leave I still hadn’t touched most of it as we were able to live mostly off one-income.

In that time I had come across Mr. Money Moustache’s approach to an emergency fund which is basically not to have one.

The premise is that you are on your path to financial independence and saving/investing 50-70% of your income. While doing this, his idea is to invest all your spare cash and if an unexpected expense arrises you just don’t save as much that month. If it’s a big expense, your savings rate may be lower for two months but ultimately you could have your “emergency fund” working for you while you are still earning.

I agreed with the concept and thought I’d invest the spare cash. My idea was that I still had access to the money and if I really needed it I could sell some shares.

The main difference for my situation was that I wasn’t earning and we weren’t saving 50-70% of our income at that time so following this idea was flawed. Still I was confident enough in the market that I could still access the money in a pinch.

You can see where this is going…

Running out of cash

As you may have read, my husband and I took a mini-retirement where we spent 2 months in Portugal at the beginning of this year. I have since returned to work part-time but won’t be paid until the end of April. This means that our mini-retirement budget had to last us 4 months.

We did have some unexpected expenses during this time which stretched our budget and for the first time in many years we are really relying on our next pay check. It’s a surreal and unpleasant feeling. We are checking our budget weekly to make sure we are still on track.

Faulty back-up plan

We still have stocks and ETFs we could fall back on if we were really stuck but we would be selling at a 10-30% loss depending on when we’d need to sell and how the markets are currently performing.

Unfortunately with ETFs you don’t get to carry forward any losses to be used as a credit against future gains. If we did need to sell at a loss, we would sell some of our individual shares which would enable us to carry forward the loss. This is the silver lining for holding individual shares.

That said, by having our spare cash in the stock market I’m less likely to spend it. If I had the cash now I would have been dipping into it as there are a few things I have ear marked to purchase with our first pay check.

Namely, a bed frame (we upgraded to a super king size but currently only have the mattress on the floor), some non-teflon cookware (for health reasons) and some art and montessori type supplies to do some educational activities with our son.

Still lucky

All that said, it’s not wasted on me that many people were living paycheck to paycheck when this hit and lost their jobs overnight. I can’t imagine how they must be feeling especially if they have big debt repayments, big mortgages, car payments and so on. At least we live in a country where we will be supported but it must be a major stress point on top of the other added stresses of social distancing and keeping kids home.

We are very lucky to be in a position to work remotely and that the company’s we work for are keeping us on. If we weren’t we would have needed to start accessing our emergency fund at a loss.

Future plans

My husband and I are on different pages as what to do first once money starts coming back in. Mr. MH wants to invest more in the market as the prices are so low compared to before. I want to re-build a traditional emergency fund as this situation has left me feeling more vulnerable than I thought. We will likely do some combination of both.

In terms of how much of an emergency fund I would like to hold, I think maybe 1-2 months of expenses in cash.

Other than that I’m looking to put income protection insurance in place until I am fully FI. This will protect me in case of loss of income for any sickness, disability or illness. This is different to serious illness insurance which only protects your loss of income for certain illnesses. You can opt for deferred payout periods for lower premiums, similar to a deductible so depending on what I pick (1, 2, 3, 6 or 12 months for example), I may up my cash savings to cover that gap.

Alternatively, one reader suggested I use credit as my emergency cash which I may use as a safety net but even with our Canadian line of credit, the interest on that is somewhere around 7% now which would compound monthly until I could pay it back. That would be worse that taking a 10% once-off hit on a stock market loss if I had to sell at a loss to access my cash in the stock market. But food for thought.

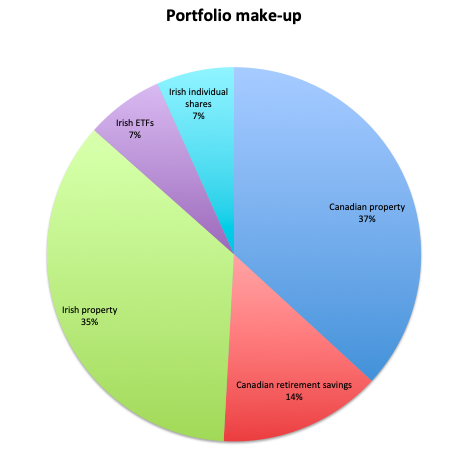

Portfolio make-up

To give you a bit of background our full net worth portfolio looks something like this:

As you can see, a large portion of our net worth is tied up in property. Our Canadian property has been costing us about 2,500€/year out of pocket to maintain after income, expenses and taxes. And that’s with full occupancy and no major repairs.

Time to sell?

We bought the condo when I was 25. Looking back, we paid too much for the it in our young naivety and were holding onto it until the markets would allow us to break even.

We have been keeping an eye on market reports and re-assessing each year whether we would sell or not. Finally one month ago, the market reports were booming and we decided to bite the bullet. We were just about to list our property when the restrictions came in.

We had already informed the tenant of our intent to sell but then had to back track as we didn’t know how to proceed with showings with the new restrictions. Then we started worrying that the tenant might decide to leave and we would be stuck for much higher ongoing costs with neither of us back to work yet.

The government in Canada is supporting it’s citizens financially, similar to Ireland but we were worried that any mortgage supports might not be available to us as non-tax residents in Canada and also that Ireland wouldn’t pay towards our mortgage costs in Canada. We would be in a bit of a grey area for financial support. This was a scary feeling.

Luckily our tenant is a member of parliament and I’m fairly certain the government pays for his rent so even though he is not currently living there, he is continuing to pay rent and not giving up the unit. The downside is that he is out of the province and cannot get back to move his things due to the travel ban and so we are a bit stuck in terms of proceeding with a sale.

What to do with the equity

Until recently my idea was to keep the proceeds of the sale in Canada and re-invest into ETFs there as it is far more tax efficient. However, upon further analysis I discovered that paying down the mortgage in Ireland with the proceeds instead would be a more favourable approach for us.

Here are the scenarios I compared:

Scenario 1:

- I go back to work full-time

- Mr. MH stay home with our son until he goes to school (something I’m still convincing him on)

- We sell the Canadian property to break even and re-invest freed up equity into ETF portfolio there

- I make nothing additional off the blog and consultations

- I do not invest through a private limited company

- We stay in Cork full-time in our current home once we reach FI

Time to full financial independence to cover 38,500€ annual expenses: 10.5 years.

Scenario 2:

- I go back to work full-time

- Mr. MH stay home with our son until he goes to school

- We sell the Canadian property to break even and bring the money to Ireland to halve our Irish mortgage

- I make nothing additional off the blog and consultations

- I do not invest through a private limited company

- Stay in Cork full-time in our current home once we reach FI

Time to full financial independence to cover 34,500€ annual expenses: 10.5 years

The main difference between the two scenarios is that:

In scenario 1:

- we keep the equity invested in Canada where tax treatment could be more favourable

- our annual living expenses only decrease by 2,500€ which we spend maintaining the property

- we have less to invest on an ongoing basis in Ireland as our annual expenses are mostly as they are now

- we need to grow our portfolio by an additional 108,000€ to cover the additional 4,000€/year in expenses

In scenario 2:

- we move the Canadian equity to Ireland paying down our Irish mortgage

- our annual living expenses decrease by almost 7,000€

- we have more to invest on an ongoing basis in Ireland as our annual expenses are significantly decreased

- we need a smaller overall portfolio to cover the revised 34,500€ in annual expenses

These difference explain why the time to full FI is the same.

The added bonuses of scenario 2 are:

- we no longer need to worry about vacancies, ongoing rental income taxes, non resident withholding taxes, unforeseen repairs and so on

- we would also save on mortgage interest, which I haven’t factored into the analysis but could be argued that savings could be invested in the stock market

- we get access to better loan to value mortgage rates

- our life insurance premiums may go down if we chose lower cover as there is less owing on the mortgage

- our annual expenses being lowered would give us flexibility to live off one income while still saving towards FI should we chose to

- alternatively, we could both work part-time and still save towards FI

- or yet another option is, should one or both of us lose our jobs we can easily get by on 2 minimum wage jobs or jobseekers allowance in a worst case scenario

We were leaning towards scenario 2 before the pandemic started for all of the above reasons, but now more than ever, with job security called into question and the losses in our stocks and ETFs we are more and more drawn to the option to cut down our expenses and reduce property ownership risks.

Even if we incur currency exchange/transfer costs and lose out on more favourable tax treatment on our investments in future, we really like the added security and flexibility having lower expenses and reduced risk would allow us.

And so, we are going to try and sell our property as soon as we can hoping we don’t miss our window while the market is still strong.

There is a shortage of housing in Ottawa and as the Toronto and Vancouver markets are over-saturated and over-priced, more investors and workers alike are looking to places like Ottawa and Montreal for better value. Boomers are also retiring and looking to downsize. All of these factors will still be in place once the pandemic is over and it will take some time for supply to catch up with demand so we are hopeful that we won’t lose too much from what we had planned.

All this to say, the pandemic has reinforced our idea to re-structure our portfolio in a way that reduces our ongoing costs and risks rather than bolstering our investment vehicles.

Investment approach

I’ve been reading a lot of articles and watching videos by different FIRE blogger’s and vlogger’s based on how they’ve been impacted and their reactions to the current crisis.

One said: “You won’t know what kind of investor you are until you experience your first crash.”

This could not be more true.

When I first bought my ETFs I experienced an 800€ loss the very next day. This was my first test. That certainly didn’t feel good but I held tough keeping in mind the historical stats and trends.

Come February I think my portfolio’s in both Canada and Ireland were up almost 15% for less than a 1 year period. That felt great and reassured me that I was on the right path to early retirement.

Fast forward a month later and I was nearly getting daily emails from Degiro stating that one ETF or another has dropped by 10%, another 10% the next day on another fund and so on. These are mandatory emails Degiro need to send with no option to opt-out.

At one point I was at a 30% loss in both accounts.

Here is a trend of how my Canadian accounts have fared since initial investment last Feb. As my Irish ETFs are loosely following the same markets the trend for my Irish portfolio would look something quite similar.

Considering:

- my Irish ETFs were technically my emergency fund

- my work contract almost got cancelled

- my husband is not due back to work until June…

This. Was. Hard!

Luckily my contract went ahead and I will be getting a paycheck in a few weeks but the experience was definitely a test.

On the one hand I was gutted not to have extra cash on hand to throw into the market when I could get ETFs on sale.

On the other I was trying not to panic. Trying not to cash out. Trying to rely on the historical trends I had read so much about. Trying to remember that anyone that cashed out in ’08 never made their money back but those that held on went on to make way more than they had put in. Trying to remember that it’s only a loss if you sell.

It was a great comfort was reading this trend report which I got in an email from my Canadian brokerage. It looks at the last 30 years of the Canadian Dow Jones of bear (down years) and bull (up years) markets and their respective gains and losses.

So far, we’ve managed to stretch our remaining cash and will rest a little easier once we have a cash cushion built up again.

The markets have even recovered quite a bit and now am at less than a 10% loss.

I am holding true to my plan and hope to invest even a small amount out of my next paycheck.

The best advice I saw was by Our Rich Journey and that was to stick to your plan. If you were going to invest 1,000€ this month, invest it. Saving towards financial independence is a long term game. Don’t try to wait for the market to reach rock bottom (or don’t try to catch a falling knife was a great saying I heard). Full time fund managers aren’t able to predict or time the market 85% of the time. Just stick to your plan. Stay consistent. You will win some and you will lose some, but if you euro/dollar cost average by investing consistently you will come out on top.

And if the market doesn’t recover, then we will have bigger fish to fry!

Morbid Couple Discussions

One night a few weeks ago, I was putting our son to bed and had worst case scenario thoughts swirling around my head. My husband is a higher risk as he has a pre-existing condition and I was trying to think about what I would do if he died. Where would I live, how would I manage financially, emotionally and so on. I came downstairs and we had a very morbid discussion about what the other would do if one of us died.

The outcome of the discussion was that with our current assets and life insurances in place we should be ok financially in that we could, at the very least, pay for funeral costs and continue living in our home.

But the discussion made us more determined than ever to reach our goal of financial independence so that should the worst happen we won’t have financial stress to deal with on top of the devastation of losing a spouse.

Summing up

Going forward I want to:

- Have an emergency fund of maybe 2 months in cash

- Invest any other spare cash and decrease our savings rate if needed to cover unexpected expenses

- Have income protection insurance in place to cover loss of income for any sickness, disability or illness. This is tax deductible. Check out lion.ie for more info

- Continue our life insurance to cover the mortgage and then some if I die

- Lower our ongoing living expenses by halving our mortgage and selling our Canadian property allowing us flexibility and peace of mind should either of us unexpectedly lose our jobs and we need to bridge the gap between getting access to our income protection or finding another job

- Continue investing in ETFs in Ireland as we build towards our financial freedom goals.

As ever, I hope that provided some food for thought. How have you coped with the market volatility and has it impacted your plans going forward? Let me know in the comments below.

Good post. Investing is about managing emotions. It is difficult to plan and invest when the future is in certain and the economy is so damaged. Global trading is about to re-balance, etc States will print and accumulate huge debts, saving will likely devaluate, etc. But, as you say, if we look back at the history there are good examples to look at and learn from.

You forgot the third scenario: Both of you die from COVID.

Problem solved, our kid would instantly be financially independent, orphaned, but Fi at 1 lol

Hi there!! I’ve just come across your blog and want to sincerely thank you for sharing such comprehensive, honest and hugely valuable Content and insights. I’ve recently discovered the concept of financial independence and was finding it super difficult to find any Irish specific content. Will 100% be an ongoing avid reader of your blog. Wishing you all the luck in the world on your financial journey. 🙂

Thanks so much 🙂 Glad the content is of use. And thanks for the well wishes.

Hi Megan, in the scenario where you sell your canadian property and use the money to reduce your mortgage in Ireland, have you considered the 33% remittance tax you would need to pay on the proceeds of the sale?

Yup, we didn’t make much of a capital gain and will have already paid 25% in Canada so the additional 8% on the small gain we made isn’t going to break the bank.

Great post!

You mentioned “re-invest into ETFs there as it is far more tax efficient.” – Is it possible for an Irish person to open a brokerage account in Canada purchase ETF’ s to avail of the lower tax?

I have a US brokerage account but they stopped offering ETF’s to Irish people about 2 years ago. I was wondering can I open a Canadian account and buy ETF’s?

Hi Brian, I don’t think it would be a runner as the tax-efficient options require you to be a resident in Canada ie: tax-free savings (TFSA) accounts for post-tax savings and registered retirement savings plans (RRSP) for pre-tax employment savings. If you lived there and had an RRSP, you can still keep that vehicle upon return to Ireland to grow money tax-free until withdrawal but the TFSA stops adding contribution room when you leave the country and is no longer tax-free under the Irish double taxation agreement, so you’d lose out on all benefits and lose to currency exchange risk and fees etc. While I think it’s important to optimise taxes where possible, I’ve somewhat stopped looking for loopholes and accepted that it’s probably much of a muchness and less headache for maintenance in the long run to just have everything here in Ireland.