Average Irish Mortgage and Interest

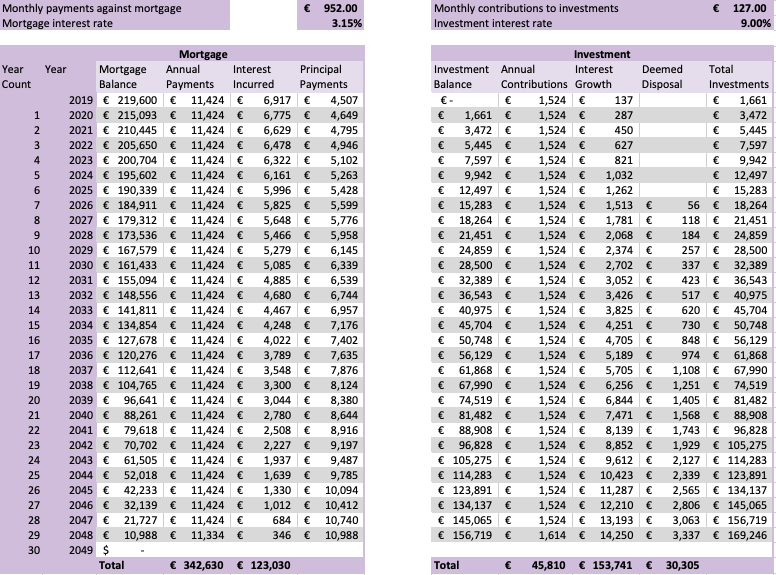

According to the Central Bank, in 2017 the average mortgage loan size for first time buyers was 206,216€ and 232,275€ for second and subsequent buyers. While the average interest rate in 2018 was 3.15%. Taking an average of 219,600€, the total interest over 30 years would come to 123,029€.

Assuming a 10% downpayment, that means that on average homeowners are paying 367,030€ for a house worth 244,000€. That’s a big chunk of change!

Traditional Advice

When I took out my first mortgage I was told to make bi-weekly payments instead of monthly and to max out the mortgage and make lump sums as much as possible in order to reduce this figure and for a long time I believed this was the best way, until I did the math myself (many years later)!

Going Against the Grain

What I found was: by taking the longest possible mortgage available to you (say 30 years) and making the absolute minimum payments you can make WHILE investing just 127€/month into a self-directed investment account at the same time at an interest rate of 9% minus the 8 year deemed disposal* (feel free to subscribe for future posts on how to achieve this :)), you can completely cancel out the 123,030€ in interest AND end up with assets worth what you paid rather than something worth 123,000 less than what you paid (with the assumption your house neither increases or decreases in value over that time).

* Deemed disposal is a tax legislation for Irish and EU domiciled ETFs where you need to pay 41% on any gains 8 years after the gain was made whether or not you have actually sold any funds. You may pay for this tax however you wish but for my analysis I am assuming you have no extra funds available outside of your investment and the tax will come out of the investment fund reducing the overall growth rate.

Now many of you are probably thinking, I live pay check to pay check and I don’t have 127€ to spare but according to the Central Stats Office’s 2015 detailed household income and expenses survey the average household with a mortgage takes home 4,980€/month and spends 4,628€/month – this should leave 352€/month to spare (or 176€ each per couple).

I know these are averages which may not apply to you but if you follow along, I hope to help you find ways you can come up with this extra dough as well as guide you on investing using my own funds as a guinea pig.

No Gain Without Risk

Now I know there is a psychological element here as well where people want to own their own home outright without owing the bank to hedge against future interest rate hikes, but if you are investing at the same time the interest in the investments usually rise with mortgage rates too. At the end of the day though you need to decide what you personally are comfortable with BUT I hope that this gives you something to consider should you wish to take a little risk in order to maximise your return on your hard earned cash!

Math Warning!

And now for the math for those that are interested. With a 30 year mortgage at 3.15% the monthly payments are about 952€ (annual totals detailed below in the column on the left). If you invest 127€/month or 1,524€/year at a rate of 9% (the historical average return of the stock market) – you will end up with interest which equals the interest paid on your mortgage over the 30 years. See interest on the mortgage table = 123,030 and interest growth minus deemed disposals in the investment column = 123,426 (153,741-30,305).

So to compare: if you just pay off your mortgage without investing along side you would end up with an asset worth 244,000€ for which you paid 367,029€ (including 10% downpayment) vs. paying off the mortgage as slowly as possible while investing and ending up with assets worth the same as what you paid out – 412,840 paid out (342,630 mortgage payments + 45,810 principle investments + 24,400 downpayment) vs final assets of 413,246 (244,000 house + 169,246 investment).

I did not account for inflation as both the mortgage payments and investment amounts will be with future money which will include inflation amounts on both sides.

Another option if you had the extra cash would be to make one lump sum investment of 17,200 at the beginning of the 30 year term which would also achieve the same result and leave you with assets worth 384,274 (244,000 house + 140,279 investments) where you paid out 384,239 (342,639 mortgage + 24,400 downpayment + 17,200 initial investment).

Summing up here are the 3 scenarios along with the total cost to you and the total assets after 30 years.

What do you think? Would you consider lowering your mortgage payments and extending your timeframe in order to invest along side? Feel free to comment below.

Still not convinced? Read on to see how paying down your mortgage in full as quickly as possible before investing could cost you almost 4 years of your life.

1 thought on “How to cancel out your mortgage interest with just 127€/month”