If you’re lucky enough to have amassed enough money to put down a 20% downpayment you may want to think twice about lumping it all against your mortgage (like I mistakingly did).

In this post I will look at 3 scenarios to demonstrate which option makes the most money sense.

Assumptions:

- There is a total of 3,025$/month to split between mortgage and investments

- House price is the average for Ottawa-Gatineau and Montreal of 241,208 as of Q4 of 2016

- 48,241$ available to use as a downpayment (20%)

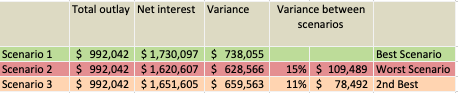

- All scenarios have an outlay of 992,042$ after 25 years

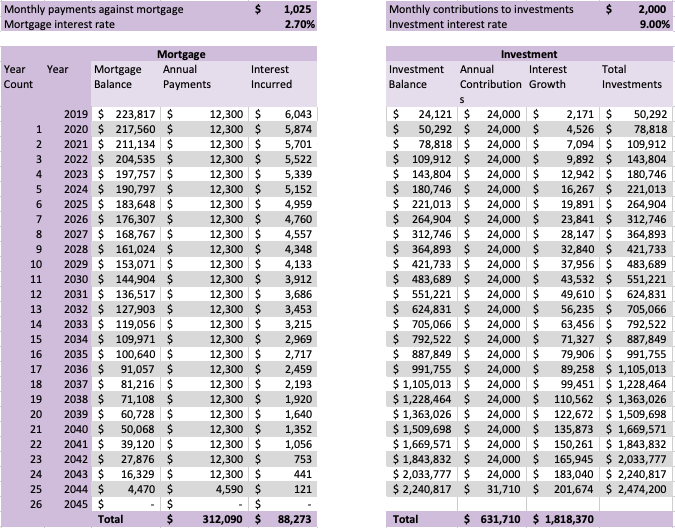

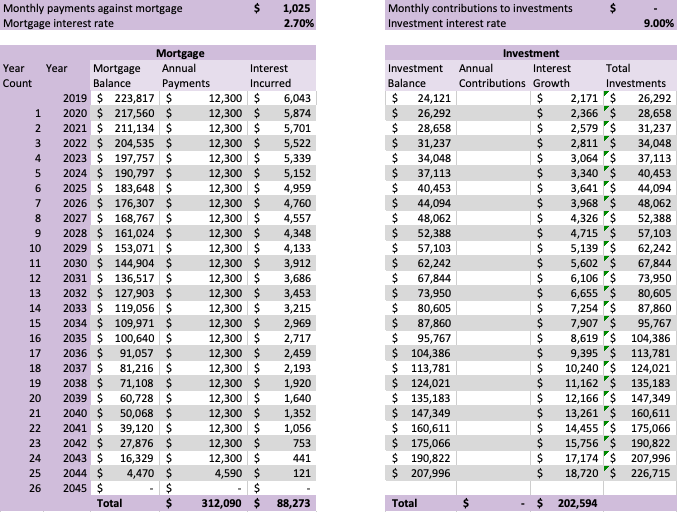

Scenario 1:

- 24,121$ (10%) is used as downpayment

- Remaining 24,121$ is invested

- Monthly payments = 1,025$ over 25 years

- Interest rate is 2.70% (lowest I could find for this type of mortgage)

- Investment of 2,000$/month is made

- Investment makes 9%

- This mortgage includes an additional 6,370$ charge for the Canadian Mortgage Housing Corporation’s (CMHC) mortgage default insurance which is charged for all down-payments of less the 20%.

Note the 6,370$ CMHC insurance is cancelled out in the first 2 years of investment growth in this option.

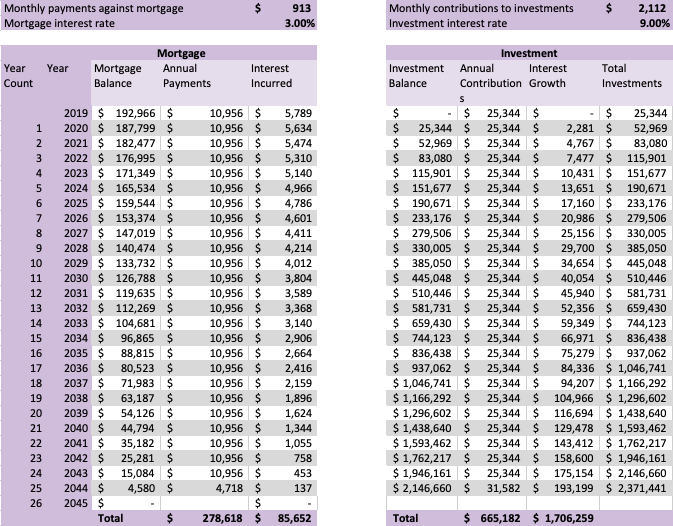

Scenario 2:

- 48,241$ (20%) is used as downpayment

- Monthly payments = 913$ over 25 years

- Interest rate is 3.00% (lowest I could find for this type of mortgage)

- Investment of 2,112$/month is made (3,025$-913$)

- Investment makes 9%

- No CMHC insurance charged

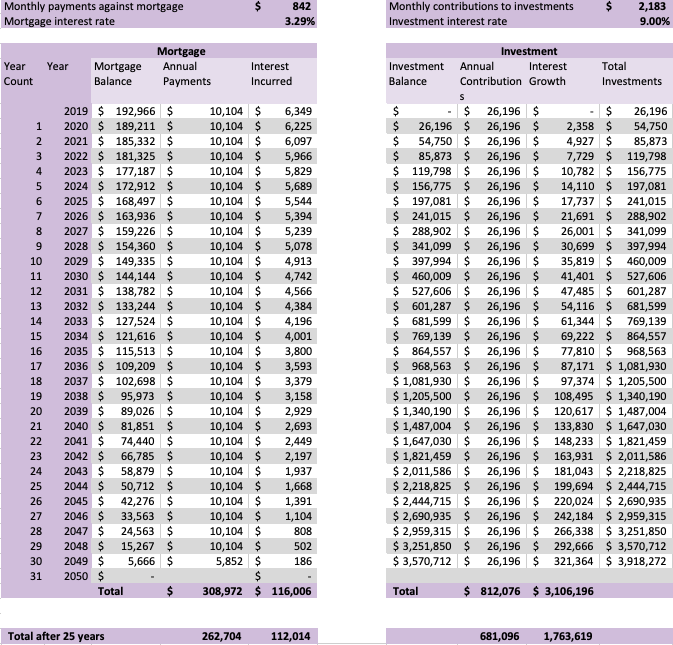

Scenario 3:

- 48,241$ (20%) is used as downpayment

- Monthly payments = 842$ over 30 years

- Interest rate is 3.29% (lowest I could find for this type of mortgage)

- Investment of 2,183$/month is made (3,025$-842$)

- Investment makes 9%

- No CMHC insurance charged

Outcome

Even though the mortgage payments are more and there is an additional 6,370$ of CMHC insurance in scenario 1, it still wins out by 15% (109,489$) more than scenario 2 and 11% (78,492$) more than scenario 3.

And even though the mortgage rate is higher for scenario 3 than scenario 2, it still makes sense to pay the lower amount leaving a higher amount to invest along side as in the end scenario 2 is still 5% (30,998$) worse than scenario 3 after 25 years.

When I took out my first mortgage I saw the 8,000$ extra that the CMHC was going to add to the mortgage with a 10% downpayment and the lower monthly payments resulting from a 20% downpayment but did not know much about investing at the time so did not look at the full picture until now. I also made multiple lump sums against the mortgage over the years and so am now considering taking out the extra equity and investing it instead even though it will increase my monthly payments and interest. The added bonus of additional interest is that, as I currently rent out the condo attached to that mortgage, I will also be able to use the additional interest as a tax deductible.

Another thing to consider for scenario 1 is that even if you do not make any further monthly contributions and only invest the initial 24,121$ you will still end up with 114,321$ net interest (investment interest minus mortgage interest paid) or assets worth 107,591 more than you put in (total assets 467,923 (241,208 house + 226,715 investments) minus total outlay 360,332 (312,090 mortgage + 48,241 downpayment and initial investment))

What do you think? Did the results surprise you?