Table of Contents

How I Decided

*Fact sheets updated for 2021

Why ETFs

Firstly a little about ETFs (exchange traded funds). These are essentially funds that bundle a large number (sometimes thousands) of individual stocks, commodities and or bonds under one fund so that you can easily track the trend of the whole stock market with only a handful of ETFs. This makes it easy for passive/lazy investing over longer terms. ETFs also offer low expense ratios and fewer broker commissions than buying the stocks individually. Historically since the inception of the stock market returns have averaged 9-11% so by having a well diversified range of ETFs you can also achieve these levels of returns with little effort.

Why not one simple ETF

After reading many blog posts about various portfolio options I settled with a slight variation to the Escape Artists suggestion explained in full detail in this post. Some bloggers suggest a very simple portfolio where you just chuck whatever money you have whenever you have any extra into one Global ETF fund like the Vanguard All-World fund (VWRL) but the reason I decided against that approach is because that fund is heavily invested in US equities (54%) and I wanted something that was a bit more diversified. According to the Escape Artist, US equities may be overpriced at the moment which may doom long term investors to under-performance (ie: when you buy high you’d need to make massive gains to make up the same returns you would if you had bought low and made smaller gains).

Why 100% stocks and no bonds

Depending on your risk tolerance you may want to put a portion (say 30 or 40% for more conservative or 90% for less conservative) of your portfolio into bonds as these have less risk but lower returns, something like the BMO Aggregate Bond Index ETF (ZAG) but as I have time on my side to let my investments rebound from any downfalls, I decided not to keep any of my portfolio as cash or in bonds. I’m open to the higher risk of a 100% stock portfolio.

Who is this for?

Therefore this portfolio mix is probably for people very early in their investment journey who have many years of contributions ahead of them before they are able to retire.

Once you are about 5 years away from retirement you’d probably want to invest in something like 30% or 40% bonds and 60% or 70% stocks with higher yields/dividends rather than higher returns.

Portfolio Make-up

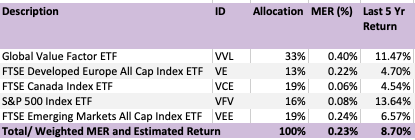

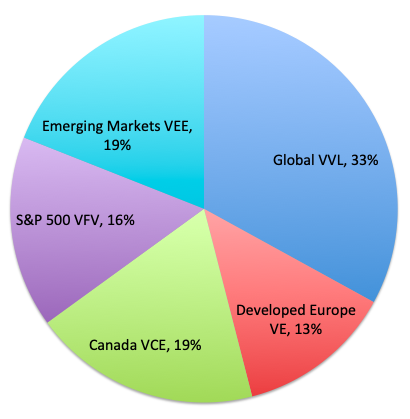

Below is the make-up of my current Canadian portfolio. All these ETFs are with the Vanguard company (See more about them below). 33% is in a Global fund, 19% in a Canada fund, 19% in Emerging Markets, 16% in the S&P 500 and 13% in Developed Europe. These funds all have varying management fees but this make-up comes to a weighted MER of 0.23% with an estimated weighted return of 8.7% based on each funds’ last 5 years returns.

And in chart form…

About Vanguard

I like Vanguard because their core purpose is “to take a stand for all investors, to treat them fairly, and to give them the best chance for investment success”, their average expense ratio is 0.10% as per 2018 assets under management. As per their website: “Vanguard is owned by its funds, which in turn are owned by their shareholders. Vanguard’s ownership structure means we have no conflicting loyalties. It’s in everyone’s interests—our clients’ and thus ours—to uphold the highest ethical standards every day. When making decisions, we are guided by a simple statement: ‘Do the right thing.'”

ETFs in Detail

Each ETF comes with a fact sheet which you can download from your Questrade account. Below are the highlights of my portfolio make-up so you can get a sense of the range of companies I’m invested in.

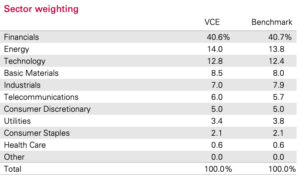

FTSE Canada Index ETF (VCE) – 19% of portfolio

This one is only invested in 64 companies where the top 10 make up 40% of the fund. The dividends on this fund are paid quarterly.

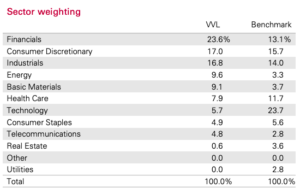

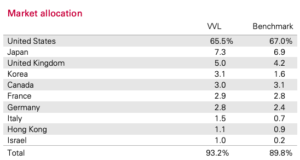

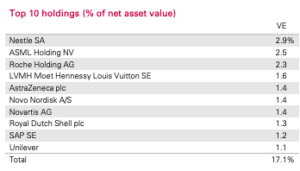

Global Value Factor ETF (VVL) – 33% of portfolio

This is a much larger spread with investments in 1,135 companies where the top 10 listed only make up 5.1% of the fund. The dividends on this fund are paid annually.

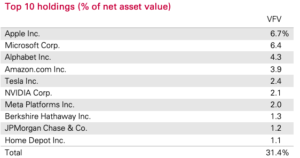

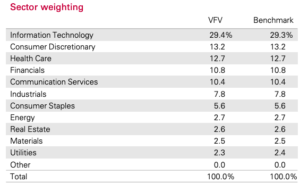

S&P 500 Index ETF (VFV) – 16% of portfolio

This one is made up of 512 companies where the top 10 make up 31.4% of the fund. The dividends on this fund are paid quarterly.

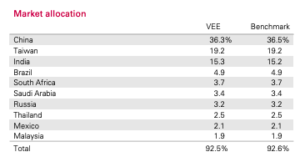

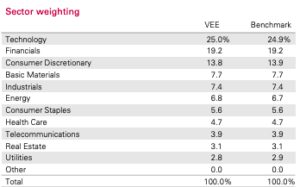

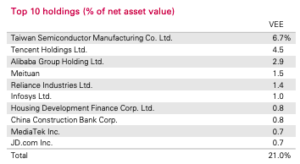

FTSE Emerging Markets All Cap Index ETF (VEE) – 19% of portfolio

This one is the biggest spread of companies with 5,256 however the top 10 make up 20% of the fund so only fractions of percentages are invested in the remaining 5,246. The dividends on this fund are paid quarterly.

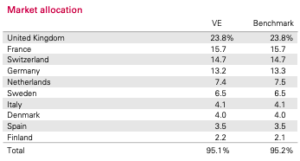

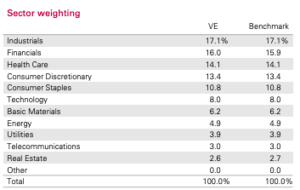

FTSE Developed Europe All Cap Index ETF (VE) – 13% of portfolio

This one is mid-sized with investments in 1,323 companies where the top 10 make up 17% of the fund. The dividends on this fund are paid quarterly.

Performance

After my initial transfer from my RRSP at the end of Jan 2019 (just shy of 3 years ago) I have since made a 40.93% gain which averages 14%/year. See growth chart below.

It’s early days but I am pleased with the results so far. This is an RRSP account so I still need to pay taxes on any withdrawals at my salary rate at time of withdrawal but it’s still performing better than it had been with my old provider.

Variations

Two other portfolio options are:

- As mentioned above a simple 1 ETF portfolio with an all world fund like the Vanguard All-World Fund (VWRL) or

- another popular make up for more conservative investors or investors nearing their retirement date would be some mix of:

- iShares Core MSCI All Country World ex Canada Index ETF (XAW)

- Vanguard FTSE Canada All Cap Index ETF (VCN)

- BMO Aggregate Bond Index ETF (ZAG)

I’ll do another post on how to purchase these in the correct proportions at a later date.

What do you think? Willing to try your hand at investing yourself? Leave a comment below.

2 thoughts on “My Canadian Portfolio”