This post took an awful lot of reading into the eye-glazing territory of pensions and a 300 line spreadsheet of analysis with varying assumptions. With so many investment options available it’s really hard to figure out which option is best to throw your money at. Hopefully this post makes that decision a little simpler.

Table of Contents

The options

First let’s look at the main pension options and how they stack up to investing on your own. Pros are in green and cons are in red. If I’ve missed anything do let me know.

| Investments | Regular company pension | Executive pension | Self administered pension (PRSA)/ Small Self Administered Pension Scheme (SSAS) |

| Available to anyone | Available to anyone in a company with their own pension scheme | Available to companies or individuals with a private limited company of which they are a director or owner. Must be managed by Trustees |

PRSA: Available to anyone, if your company does not have a pension they are required to offer one by law and a PRSA can be requested. SSAS: Available to companies with less than 12 members or individuals with a private limited company of which they are a director or owner. Must be managed by Trustees |

| Contributions are not tax deductible, only after tax money can be contributed increasing time to retirement | Can invest pre-tax money reducing time to retirement – max contribution room is a percentage of your income which grows as you age ie: 20% if you are 30-39 | Can invest pre-tax money reducing time to retirement – there is no max contribution BUT only a certain portion is tax deductible and therefore only worthwhile contributing to these limits. Limits are the same as regular pension which is a percentage of your income which grows as you age ie: 20% if you are 30-39 but up to an annual salary of 115,000€ | Can invest pre-tax money reducing time to retirement |

|

Depending on the investments you need to pay taxes on dividends and gains. For example: Shares: 33% capital gains on gains and income tax+PRSI+USC on dividends upon sale. Irish-domiciled ETFs: 41% on gains, 41% on dividends and payable every 8 years deemed disposal regardless if sold |

Money grows tax-free (no tax on gains until withdrawal) | Money grows tax-free (no tax on gains until withdrawal) | Money grows tax-free (no tax on gains until withdrawal) |

| Taxes require filing each year, may require accountant if not comfortable doing yourself | Taxes managed through company | ||

| Cannot purchase investment property using funds | Cannot purchase a property using the pension | Cannot purchase a property using the pension | Can purchase an investment property with the pension, pay no income tax on rental or capital gains on disposal but lack of diversification and expensive to setup/lending terms – more here |

| The government can introduce more charges/regulations like deemed disposals | The government can (and have) introduced a levy on pension funds | 0.9% levy applies | The government can (and have) introduced a levy on pension funds |

| Withdraw at any time | You are not allowed to drawdown funds until the age specified by your company. Can be anywhere from 55-70. This means you need some form of savings to get you through from your financial independence/ retirement date to the earliest date your pension can vest. | You are not allowed to drawdown funds until 50. This means you need some form of savings to get you through from your FI retirement date to the earliest date your pension can vest. | You are not allowed to drawdown funds until 60. This means you need some form of savings to get you through from your FI retirement date to the earliest date your pension can vest. |

| More flexibility: can choose what to invest in | Less flexibility when it comes to investment choices, limited to the funds available with the pension provider | Less flexibility when it comes to investment choices, limited to the funds available with the pension provider | More flexibility in what you invest in but still need to have it managed by a fund manager or stockbroker, reducing returns |

| Free to take your money where you want | Less flexibility to transfer your pension fund abroad compared to regular savings | Less flexibility to transfer your pension fund abroad compared to regular savings | Less flexibility to transfer your pension fund abroad compared to regular savings |

| The tax regime could change in Ireland (tax risk) | The tax regime could change in Ireland (tax risk) | The tax regime could change in Ireland (tax risk) | The tax regime could change in Ireland (tax risk) |

| No income tax upon withdrawal | PAYE, PRSI and USC are due on any withdrawals at rate of income at time of withdrawal. Though if you only require 16,500€/year per person you effectively pay no income tax and only 4.9% for PRSI and USC as per current credits | PAYE, PRSI and USC are due on any withdrawals at rate of income at time of withdrawal. Though if you only require 16,500€/year per person you effectively pay no income tax and only 4.9% for PRSI and USC as per current credits | PAYE, PRSI and USC are due on any withdrawals at rate of income at time of withdrawal. Though if you only require 16,500€/year per person you effectively pay no income tax and only 4.9% for PRSI and USC as per current credits |

| Take money out when you want it, how you want it | Complicated retirement options of tax-free lump sums, annuities or approved retirement funds each with their own restrictions/ guidelines to weigh up – some even include a mandatory withdrawal rate of 4% which risk your fund running out of money | Complicated retirement options of tax-free lump sums, annuities or approved retirement funds each with their own restrictions, guidelines to weigh up | Complicated retirement options of tax-free lump sums, annuities or approved retirement funds each with their own restrictions, guidelines to weigh up |

| Fees depend on what you invest in, low cost ETFs or Investment Trusts can significantly increase your returns outweighing all other disadvantages | High management fees resulting in less return on investment outweighing all other tax advantages | High management fees resulting in less return on investment outweighing all other tax advantages | High management fees resulting in less return on investment outweighing all other tax advantages |

|

For example: 1.25% up to 100,000, 1% between 100,000 and 1 million and 0.75% over 1 million for PRSA 0.50% for SSAS |

|||

| Costs to setup: Between 2,000 and 3,000€ including unit trust setup and legal and conveyancing fees |

The deciding factor

Although pensions appear on the surface to be much more tax efficient than investing in Ireland, it ends up that all of those incentives are wiped out by very convoluted fee structures which decimate your real rate of return and reduce your end investment.

A very detailed report was carried out by the Department of Social Protection in 2012 on the pension charges in Ireland and summarised that there are “a wide range of issues in relation to pension charges and identified a number of serious problems. It is clear that there are major challenges to be addressed in the two main areas of transparency and reasonableness of charges. The report fully accepts that pension savings cannot be cost free. However, it appears very clear that consumers do not understand that even a modest charge can have a very large impact on the final pension.”

The OECD gave a guideline that for every 0.25% of a fee on your portfolio results in 5% less in your end portfolio amount.

Again quoted from the above report: “This can be illustrated with the following: If an individual age 35 saves €250 per month for a pension for 30 years, a fund of approximately €200,000 is created which results in a pension of about €10,000 per annum. Apply the average charge (found by the report) of 2.18% per annum to this fund and the final fund is reduced by 31% i.e. the fund is reduced by €62,000, resulting in a lower pension of €6,900 per annum. This impact would be significantly higher where the maximum charges apply.”

Hidden Fees

You may not even be able to find out the true cost of your fund either as there are often hidden charges not made available to the pension saver.

“Investment managers typically disclose annual investment management charges for the management of a pension investment mandate but this quoted annual management charge may not take into account all expenses incurred by the underlying pension fund. These are not generally reflected in reduction in yield calculations, relate to underlying costs of investment management and are known as implicit costs. These additional costs such as those detailed below, will impact long term pension values to differing degrees and are not typically disclosed to individual pension savers.

- Operational Costs (such as custodian fees, trustee fees, audit fees etc.);

- Trading Costs (typically brokerage commissions payable when an asset of the fund is bought or sold);

- Stamp Duty and other taxes (taxes related to share dealing in certain jurisdictions)

The range of additional implicit costs identified amount to reduction in yields of between 0.1% and 0.3% per annum, resulting in a further overall reduction in final pension fund value of 2% ‐ 4% for occupational pension schemes and individual pension arrangements. However, costs will depend on the underlying fund structure and can be significantly higher.”

And now for the analysis

My 300 line spreadsheet looks at the “big picture math” to properly weigh up the true impact of all of the pros and cons listed above between a pension and an investment outside of a pension.

I took the average Irish income and expenses as you may have seen in this post, and applied the full savings to 2 scenarios: saving for retirement using a pension vs investing outside of a pension.

In each case I look at how long it will take to build a retirement fund allowing for a safe withdrawal of 16,500€/year (for one person) as well as how each fund performs over the next 30 years based on a number of assumptions.

The assumptions:

Scenario 1:

Investing in pension – growth phase:

This includes some money into a pension as well as some into an investment account as the assumption is that the saver has more than the max contribution room of their pension to save each month. It doesn’t make sense to put any more than the max contribution room into your pension as you are not reducing your taxable income beyond that point and you are better using the rest of your disposable income in an account with a higher rate of return. Also if you plan on drawing income from your investments before you can access your pension, you will need investments to draw from in a non-pension account until your pension is available.

Summarised:

| Monthly investment (pre-tax €) | 716.66 € |

| Pension growth | 2.90% |

| Monthly investment (after-tax €) | 653.00 € |

| Savings growth | 6.75% |

| Total monthly savings | 1,370 .66€ |

Detailed:

- Monthly investment (pre-tax) into pension: 716.66€

- max contribution of 20% of gross income for people aged 30-39. Average salary of 43,000€ was used

- Pension growth: 2.90% real rate of return (after fees and inflation)

- based on historical average, though the report only has data from 2007 (-7.3%), 2008 (-35.7%), 2015 (4.5%), 2016 (8.1%) and 2017 (6.3%). I took average excluding 2008 as that was due to the crash which is hopefully an anomaly

- Monthly investment (after-tax) into savings: 653€

- as the average Irish household spends 40,000€ per household, I assumed an even split and said 20,000€ for one person or 1,667€/month. Take home after 20% pension contribution would be 2,320€/month minus the 1,667€ expenses leaves 653€ to invest into separate self-directed investment account

- Savings growth: 6.75% real rate of return (after fees and inflation)

- based on historical stock market average return of 9% minus 1.9% inflation and 0.35% fees for ETF portfolio

Investing in pension – withdrawal phase

Summarised:

| Pension lump-sum | 25% |

| Income tax+PRSI+USC | 4.90% |

| Investment deemed disposals | 41% |

| Withdrawal rate | 3.50% |

Detailed:

- 25% of pension taken as tax-free lump sum and re-invested into self-directed investment account

- on retirement, you can take a tax-free lump sum out of your pension to do with as you wish. The amount is limited to 25% of your fund up to a max of 200,000€. I’ve chosen to re-invest at a higher rate of return

- Pension withdrawals reduced by 4.9% for income tax+PRSI+USC

- current tax credits allow for 16,500€ salary without incurring any income tax the remaining bands of PRSI and USC for that amount come to 4.9%

- Savings account reduced by 41% deemed disposals on gains every 8 years

- assuming savings are invested in low cost Irish-domiciled ETFs, these incur 41% tax on income and 41% tax on any gains, even if you don’t sell, the government brought in deemed disposals to get access to your money every 8 years, instead of taking this off the withdrawal, I have reduced the fund value by the deemed disposal amounts. This could be avoided if you purchase shares directly but those come at higher transaction fees and can be tricky/risky to pick the right shares, so may be much of a muchness

- Withdrawal rate: 3.50%

- there are many articles about the safe withdrawal rate of 4% which essentially states that you can withdraw 4% per year from your portfolio without much chance of your funds running out. However when I tried this figure along with all the other growth assumptions and tax implications specific to Ireland, the portfolio did start losing money after a number of years and so I reduced to a safer rate of 3.5%

Scenario 2:

Investing in self-directed funds – growth phase

Summarised:

| Monthly investment (after-tax €) | 1,041.66 € |

| Investment growth | 6.75% |

Detailed:

- Monthly investment (after-tax) into savings: 1,041.66€

- as the average Irish household should have 25,000€ to spare after expenses, I assumed an even split and said 12,500€ for one person or 1,041.66€/month

- Savings growth: 6.75% real rate of return (after fees and inflation)

- based on historical stock market average return of 9% minus 1.9% inflation and 0.35% fees for ETF portfolio

Investing in self-directed funds – withdrawal phase

Summarised:

| Investment deemed disposals | 41% |

| Withdrawal rate | 3.50% |

Detailed:

- Savings account reduced by 41% deemed disposals on gains every 8 years (see above for more details on this)

- Withdrawal rate: 3.50%

Phew!

The results

If I haven’t lost you, fair play as that’s some pretty eye-glazing stuff but here is how it all played out:

| Pension | Investment | Variance | |

| Years to retirement | 18* | 19 | 1 |

| Starting portfolio | € 446,786 | € 442,054 | -€ 4,732 |

| Starting annual withdrawal | € 16,214 | € 16,516 | € 302 |

| Ending portfolio | € 480,500 | € 511,133 | € 30,633 |

| Ending annual withdrawal | € 17,562 | € 19,097 | € 1,535 |

| Total return | 8% | 16% | 8% |

*from year 16, contributions to the savings account were no longer needed to reach the final comparable amount (but still contributing to the pension).

So as you can see, even though there were tax incentives to save towards a pension, it didn’t make much of a difference in the years to retirement as the growth of the pension was much lower than the investment account, even with the 41% deemed disposals taken into account!

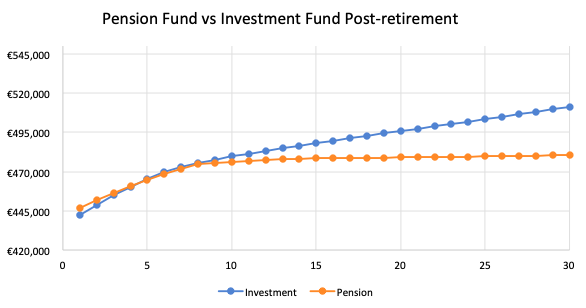

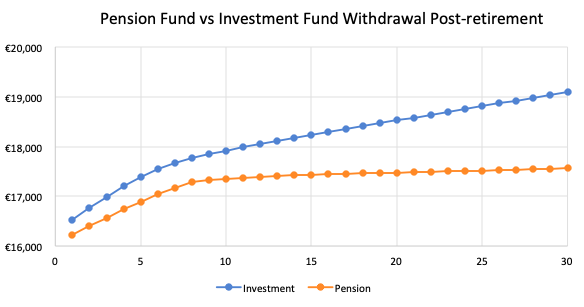

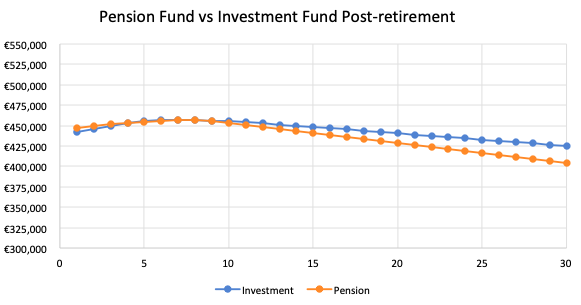

And now for some graphs:

Investment growth in blue and pension in orange. Over 30 years the investments outperform the pension.

Similar trend to your withdrawal rate where you can withdraw more year on year from the investments than from the pension.

So based on all of the above assumptions the winner is to invest outside of a pension as long as the rate of return is higher. Plus the major bonus is that you are not subject to all of the rules and regulations with your pension and you can access your money at any age in an investment account.

Like everything else I’ve analysed to date, it all comes down to your rate of return in each scenario, aside from all other assumptions this seems to be the overriding factor of success.

But what if…

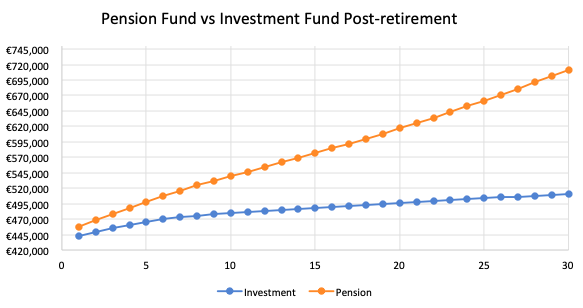

For arguments sake, what would happen if the pension account made the average return it has made from 2015 to 2017 of 6.3%?

Well then the pension wins by far and it takes 2 fewer years to reach retirement (16 years). You also end up with 184,000€ more in your portfolio after 30 years compared to the investments and 6,700€ more in annual withdrawals.

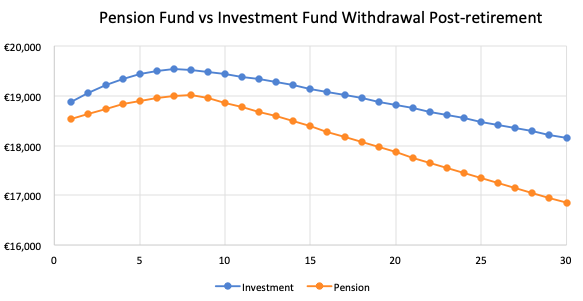

And that withdrawal rate?

For illustration purposes, if I put in a withdrawal rate of 4%,, although you reach retirement 2 years sooner in both scenarios, you end up dipping into your principal 15 years after retirement, and while your pension doesn’t get to zero, your annual withdrawals start to reduce by almost 2,000€ less per year at the end of 30 years.

AND that’s a wrap! If you’ve made it this far you deserve a drink 🙂

Food for thought

While we’re on the subject of pensions.

The state pension is currently 12,900€/year and only available at 66 years of age which has already been pushed out to 68 by the year 2028 and with the population aging and fewer people contributing I wouldn’t be surprised if other major restrictions are brought into place.

If the current average spending per person is 20,000€ year that’s a 7,100€ gap per year. You’d need 193,500€ saved in order to draw that gap down at a 3.5% withdrawal rate. With the average pension contribution of 4% (1,799€/year or 150€/month) it would take 49 years to save up that amount at a growth of 2.9% or 31.5 years at a rate of 6.75% (if you’re starting from zero).

As we saw above, if you boost your savings to 1,000€/month you could have enough to withdraw 16,500€ in 19 years time. So if you’re 35 now, you could still retire by 54, or at least be financially free to do what you wish with your time, be that reduced work weeks or find a job where you can work remotely from a beach during the winter. That’s still 14 years sooner than you’d have access to the state pension.

What do you think? Leave a comment below if I’ve missed anything or if you’d like to see any more analysis like this.

Hi just discovered your blog after hearing you on the Irish fire podcast. I have read all you posts over two days and it is simply brilliant, really clear and considered analysis and very enjoyable to read.

Just a quick question on the above. Does your analysis take the 40% tax savings on contributions into account. The monthly 716 only costs you 429 in reality

Hi Martin, Ah great, glad you’re enjoying the blog. Yup the scenarios do take into account the 40% tax savings. I tried to compare very similar scenarios. Both looked at someone earning 43,000€ saving the average 12,500€ after-tax per year as per 2015 CSO household survey. Scenario 1 has the person investing 716 of pre-tax money (which is the max contribution they can make of 20% for age 30-39) PLUS 653 in after-tax money into ETFs. Meaning they get to invest 16,447€/year while the person investing only after-tax money is investing 12,500€ each year. It’s not a clear 40% more as you can only invest a max of 20% of your salary from age 30-39. Hope that makes sense?

Great writeup. Usually people assume pensions are always better due to not having income tax applied and they stop there. Great to see someone apply this to the actual return.

I’m trying to build such a spreadsheet myself at the moment. Any chance you could post it?

For the self invested scenario with ETFs, does the above take into account capital gains tax applied on the ETF after 8 years, then reinvested and taxed again after another 8 years etc.

Or maybe I misunderstand? I’ve been assuming you would be double/triple taxed again at year 16/24?

Hi Eoin, Thanks! Funny you should ask. I actually just launched a member’s area with access to all my templates. Due to the amount of time it took to build it, I have put it behind a paywall but there are a decent set of tools in there to help with your analysis to help you find your own path to financial independence. You can see screenshots and such here before deciding. https://mrsmoneyhacker.com/member-area/

Also yes, the analysis includes the 8 year deemed disposal. You are not double taxed. You are only charged on the gains from year 1 in year 8 and the gains from year 2 in year 9 for example so you only ever pay the tax once. When you actually sell, the taxes you paid in previous years also act as a credit.

Hi Megan,

As mentioned above, great write-up!

On this point however, you mention – “You are only charged on the gains from year 1 in year 8 and the gains from year 2 in year 9 …”. I find this conflicts with my current understanding after reading documentation elsewhere on the web.

My understanding was that you pay the accumulation of all growth that occurred from years 1 to 8 when you reach year 8, assuming you have not sold off your position.

Then, when you eventually sell off your position – say after 20 years, you are taxed 41% of the total gains made minus any deemed disposal taxes you had paid during your holding.

Would like to hear your take on this 🙂

Thanks Again!

Hi Shane, Thanks for reaching out. What I wrote in that post is wrong, I need to update it 🙂 I have since learned a bit more about it and documented my latest understanding here. https://mrsmoneyhacker.com/how-to-file-taxes-for-etfs-in-ireland/. Your understanding is correct, though the growth you pay tax on is only the growth from year 1 to 8 on the ETFS you bought in year 1, not the growth of all ETFS bought between year 1 and 8 if you get me.

Hi Megan,

The math here is loosely based on a pension fund returning 2.9% with “high management fees” and an Investment Portfolio returning 6.75%.

I believe pensions have changes a lot since 2012 (wow, almost 10 years ago), and I think that a modern pension scheme will definitely outperform an Investment Portfolio. Here is why:

– Pension Schemes have access to passive ETFs – that is, the pension returns can match (before fees) that of an Investment Portfolio. If you were to match the return rates in your spreadsheet, how would that change the picture?

– “High management fees” are not that high anymore – my pension fund of choice (a passive all world ETF that tracks the FTSE All World Index) has an Annual Management Charge of 0.3%. This means that my pension will lag the above Investment Portfolio by 0.3% only. This is a substantial difference to the figures used above (where pension return halved).

Do you think we could get a “Pensions vs. Investments Revisited” post to see how the math holds up? Thanks

> what would happen if the pension account made the average return it has made from 2015 to 2017 of 6.3%?

I see this now. However, I still think this deserves a post of its own. Thanks

Hiya, yes definitely if you can get a pension that performs well and has low fees then it can outperform an ETF portfolio outside of a pension. That said, the vast majority of people including clients of mine, are not in these pensions. There is so little financial education and hands on approach to managing a pension in the every day world. I’d actually be very surprised if the only fee you are paying is the 0.3% – this is likely the fund management charge only, there are likely other hidden fees like annual management charge (for operating the pension), commissions (which can be up to 50% for the first 2 years of contributions), bid/spread offer (when you actually sell/withdraw), allocation rates etc. All of these combined can completely negate any tax deferral savings and they are very good at hiding them. You also have the disadvantages of a pension too in terms of restrictions on access age, potential levies being applied by government (as they did previously) and other limitations/complications once you actually go to withdraw (there are added fees there too to convert to an ARF or annuity). For me, it’s very hard to buy into a pension given all of these issues but they can definitely make sense for many people.

I thought deemed disposal does not apply to Pension investments – including ETFs purchased in PRSAs?

Hiya apologies for the delay. As far as I know deemed disposal for ETFs still apply in a pension but it’s just managed by the fund itself.

Deemed disposal does not apply to pensions. Pensions are allowed to grow tax free.