This post goes into the psychology of money, the recipe for human happiness as well as ways you can use this knowledge to build a sustainable budget without impacting your happiness. You can also view this on YouTube.

Table of Contents

Happiness is relative

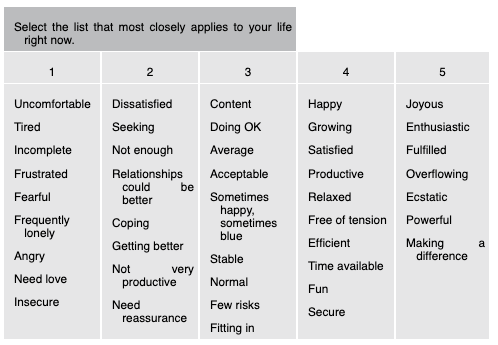

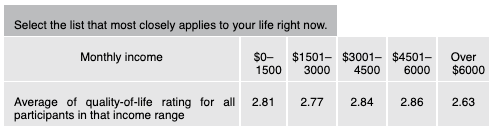

Vicki Robin, author of the New York Times bestseller Your Money or Your Life, began running finance seminars back in the 80’s. In them she would ask the audience “how much would it take to make you happy,” almost everyone, in every income bracket, said “double what I am making now”. Then, when asked to rate their happiness on a scale of 1 to 5 (scale and ratings below), there was no significant difference between the top and bottom earners. You could hear a pin drop as people realized that the person in the row ahead of them probably had the “more” they thought would make them happy—and it made no difference.

Nobel laureate and best-selling author Daniel Kahneman, in his research on money and happiness, found that beyond a certain level of sufficiency (currently about $75,000 a year in the United States), more money doesn’t buy more happiness.

Understanding this can help you to start changing your mindset around money and consumerism, in order to really cut back on spending in a sustainable way and help you to work towards financial security where you will have more freedom to spend time on the more important things in your life.

Recipe for human happiness

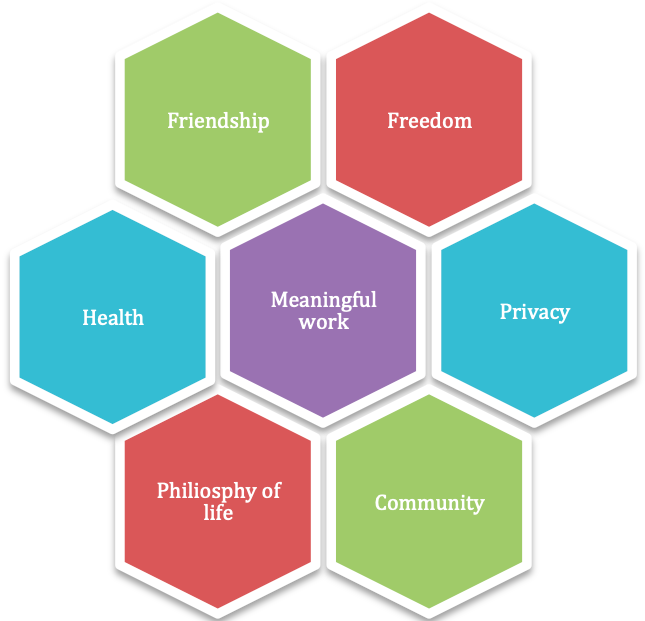

Below is a graphic of the main components different psychologists have found to be the recipe for human happiness.

Ask yourself, how many of these things cost any money? Certainly money can help you be more comfortable but once your basic needs are met, instead of spending money on material things, you could invest that money and spend the time it buys you on the real things that bring you happiness.

Also, have a think about your perfect day and the top 10 things you do on a weekly basis that bring you the most happiness. How many of these cost some or any money?

In the documentary Playing with FIRE, a young couple, consumed by the idea of the American dream, lived in an expensive house by the beach, drove expensive cars, had expensive things, but were so stressed and tired they had no time to do the things they loved. They took a step back and did an exercise where they asked each other to write down 10 things that brought them the most joy.

They included things like:

- Hearing their baby laugh

- Having coffee together

- Baby cuddles

- Going for a walk

- Going for a bike ride

- Enjoying a glass of wine

- Good chocolate

- Talking to parents and family

- Family dinners

- Reading to their baby

When they really looked at that list, they realised none of those things:

- included going to the beach (which they pay a premium for)

- included the cars they spend so much of their working lives paying for

- were location-dependent (they could do those things anywhere)

Ultimately, they sold their house and moved somewhere cheaper and the documentary chronicles their experiences on their path to financial independence.

What’s on your list?

Hedonic treadmill

The hedonic treadmill explains why when you buy something, the joy you experience from that item is short-lived explained further below.

Spending on experiences vs stuff

Ever bought a big ticket luxury item say, a new car? Or even something smaller like a new phone? Did it make you feel good? That’s because your brain detects these purchases as a positive change to your life and releases a hit of dopamine, the pleasure hormone. Then did you notice how your happiness with the new item is short-lived? This is because your brain reacclimatizes it’s baseline and the next time you buy a similar item, your brain expects to feel the same sensation but since you’re expectation has increased, you don’t feel the same level of pleasure. The same thing happens with drug users chasing their first high.

As time goes on, the longer you own the item, the less happiness it brings as you need to insure it and maintain it, and not get any additional hits of dopamine for it. The more stuff you own, the unhappier and more stressed you will be.

Experiences are different

Each experience is different, bringing a new high each time, and you create memories that you can look back on and re-experience that same high.

The more you spend on experiences like travel and learning new skills, the happier and more content you will be.

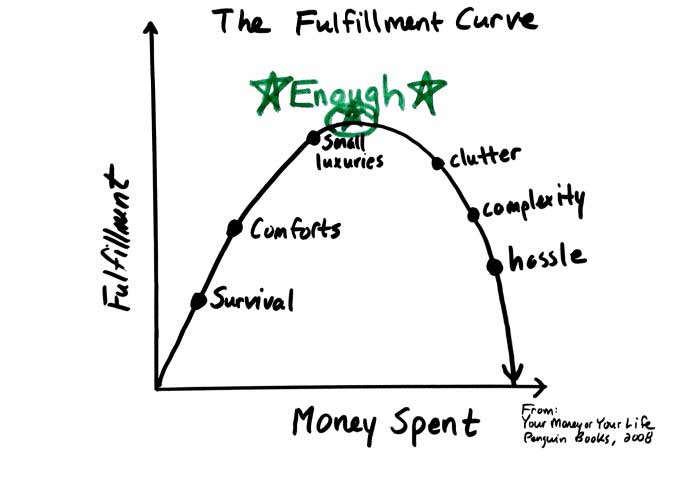

Fulfillment curve

The concept of the fulfillment curve is that once you have enough necessities for our survival, enough niceties for your comforts and pleasures and even enough little “luxuries” we have everything we need. Everything outside of that is excess and actually starts to weigh you down. Taking time, effort and cost to maintain. Having more than “enough” starts to diminish your sense of fulfilment from those items.

Lifestyle inflation

Lifestyle inflation refers to an increase in spending when your income goes up. Lifestyle inflation tends to become greater every time a you get a raise and can make it difficult to get out of debt, save for retirement, or meet other big-picture financial goals.

Being aware of this can help you to avoid falling subject to this.

The way you should look at increases in income is not what other material objects can I buy, a bigger house, a nicer car but instead how much TIME in my future can I buy if I invest this instead.

Personally, we are earning more than we ever have but our expenses have stayed about the same and it has enabled us to live the lifestyle mentioned in earlier posts.

Lifestyle is really well explained by these to graphs as detailed on this post

Average Joe increases his spending with every raise meaning his savings rate never really increases and essentially means that without state aid, will never be able to retire. Extraordinary Joe keeps his expenses the same regardless how much he earns, enabling him to save and grow his spare cash through investments, allowing him to reach retirement or even financial freedom MUCH sooner.

Creating a budget that is sustainable and increases happiness

So how do you use this knowledge to crate a sustainable budget that doesn’t decrease your happiness?

Different types of expenses

First, understand that there are different types of expenses:

- Baseline expenses (mortgage/rent, groceries, utilities etc) – bring neither happiness nor unhappiness

- Some baseline expenses decrease happiness like insurance or unexpected maintenance costs

- Some spending increases happiness – where something new is brought into your life – either stuff or experiences. As we’ve seen, the hit of happiness from things is temporary but much longer-lasting for experiences.

Step 1: Know where your money is going

If you don’t know exactly how much you’re spending and on what you won’t be able to identify areas to best cut back.

There are lots of tools and tricks to help with tracking expenses but it doesn’t have to be laborious. Some people like to track daily but I like to do a retrospective once every 6 months or so. This can be as simple as extracting a CSV from all your bank accounts and credit cards (though some of these only go back 4 months online), compiling them all into one worksheet in excel and categorizing each expense into a set list of main categories and sub-categories (again you could find some samples online to get you started). Once you’ve done this you can use a pivot table to sum up all the categories to really see where your money went.

Some online tools have great visual reporting and budgeting techniques and guidance. I use YNAB (You Need a Budget), Pocketsmith is another one which allows auto-syncing from your bank and credit cards. Note though that syncing your bank with a third party tool exposes you to risk and waives your protections typically covered by the bank for fraud.

Step 2: Then look at the expenses that bring neither happiness or unhappiness

For example: your baseline costs (mortgage/rent, food, utilities, insurance). Cutting down on these costs will not impact your happiness one way or the other, though they will increase your savings rate and speed up your time to financial security.

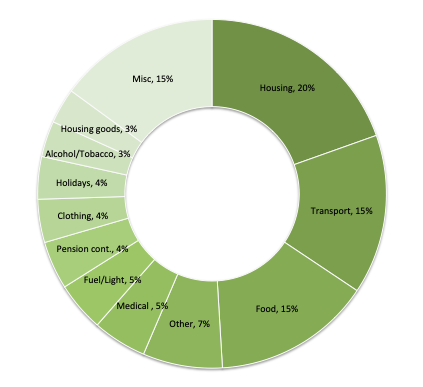

The biggest expenses in most households are food, accommodation and transport – making up 50% of household expenditure according to the latest CSO household survey in 2015.

Step 3: Next cut costs that temporarily reduce happiness

The next items to look at will be things that reduce your quality of life a little but the beauty of the hedonic treadmill is that just as new purchases temporarily increase your happiness and your baseline expectation rises to expect the same high next time, it also reduces expectations when cutting out expenses and while you will feel a temporary decrease in happiness, your happiness level returns to the lower baseline and you will not experience prolonged decrease in happiness for having cut those expenses.

Things like cooking at home instead of eating out, or buying used things instead of new are good examples.

Step 4: Next TRY to find the expenses that you THINK cannot be cut without permanently affecting your own well-being.

Try cutting them out and if your happiness baseline does not adapt then do not cut those expenses. You won’t know unless you try. You do not need to cut these out completely but even reducing the frequency could make a big impact.

They could be things like:

- Buying lunch at work

- Eating out at restaurants

- Going out with friends

- Going to live sporting, music or theatre events

Step 5: Add back in some luxuries

After cutting expenses in the other steps, you should have freed up some extra money to budget in some splurges or “fun money”. As long as the amount is less than the amount you saved by cutting in the other areas, you will still have money left over to build towards financial security but also increased your happiness, even by spending less money!

You’ll actually find, after a bit of trial and error, that you can live on quite little and actually have increased happiness without the stress of money.

Other tips for justifying expenses

Using the 4% rule, for every 100€ that you continually spend, you will need 2,500€ invested to passively cover this cost. So if you’re looking to spend 100€ on something, ask yourself how long it takes you to save 2,500€ and that is how much time you are adding to your time to financial freedom.

Another way to justify if something is worth spending on, convert costs into the time you spent to pay for it. If you’re a single person earning a salary of 50k, without applying any non-standard tax credits you take home just shy of 37k or just over 3k/month. If you want to spend 2k on a holiday that means you will have spent almost 3 weeks of your life to pay for this. If this feels worth the time you’ve exchanged for it then it’s worth it but if not, it might help you to cut back further on expenses you would have otherwise thought nothing of spending on.

Another good example is a new car: If you buy one for 30,000€ and you take home 37k/year, you’re essentially working for an entire year of your life to pay for that car.

I really enjoyed this post, thanks Meagan. Sounds like you’ve all your priorities right. Also, just finished Vicki Robin’s book a few weeks back and great to see that you’ve integrated it into your life and goals.

Steve

Thanks Steve 🙂 In terms of priorities, it certainly is an ever-evolving target ad was a LONG time getting to this point in our spend vs happiness balance but I think we’ve found the right balance for us for the moment. I just loved that book!

LOL, this year transport — 0%