Ever wondered if it was better to rent or buy on your path to financial independence? This post looks at how many years it would take to reach financial independence using average Dublin rent and house prices in 2021.

Financial independence in the context of this post refers to building a portfolio large enough that you can withdraw 4% per year to cover your annual living expenses meaning you no longer need to work for money.

I should also start by saying that the maths behind deciding whether to rent or buy is only one part of the equation. Owning your own home is a very personal choice and allows for much higher levels of customisation and control but what I want to demonstrate in this post is that owning your home is not a requirement to achieve financial independence.

Also to note that if you are not great at saving then a mortgage can nearly be a forced way for you to grow your net worth and reduce your cost of living over the long term. If you are good at saving though then the rent vs buy debate can start to be more comparable which I will demonstrate below.

Table of Contents

General Assumptions:

- Jointly assessed couple earning 100,000€ combined (68,609€ take home)

- Couple is 36 and 37 with kids

- Annual living expenses without accommodation: 36,840€ including childcare averaged at 900€/month for the full time to FI, this is averaged out over the long term to include multiple kids in creche, school and college over the years.

Buy assumptions:

- Purchase costs

- An average house price of 400,000€ – the average between North and South Dublin prices as per Daft’s latest house price trend.

- First time home buyer scheme with 10% downpayment of 40,000€

- Other purchase costs including stamp duty, legal fees, valuation, engineer estimated 8,600€

- Furniture costs: 10,000€

- Total outlays: 58,600€

- Ongoing costs:

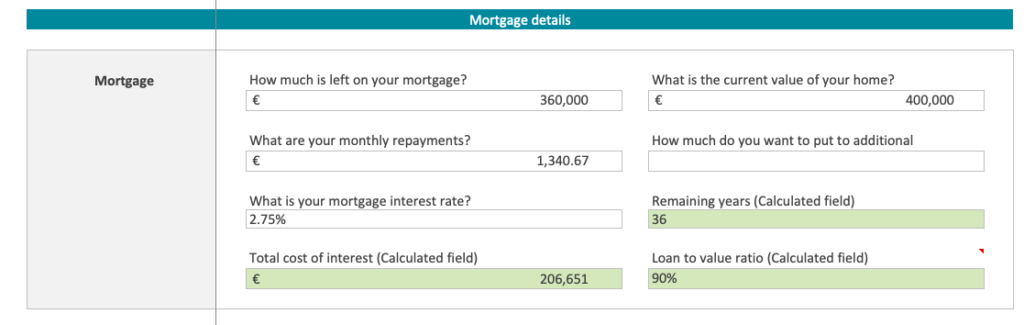

- Monthly mortgage payments: 1,341€ (16,088€/year)

- Mortgage rate: 2.75% over 36-year term

- Estimated annual homeownership costs: 4,750€ including home insurance, refuse, mortgage/life insurance, local property tax and repairs/maintenance/upgrades (estimated on average at 3,500€/year)

Total annual expenses: 57,678€

Total annual savings: 10,931€ post-tax or 15,304€ pre-tax in a pension

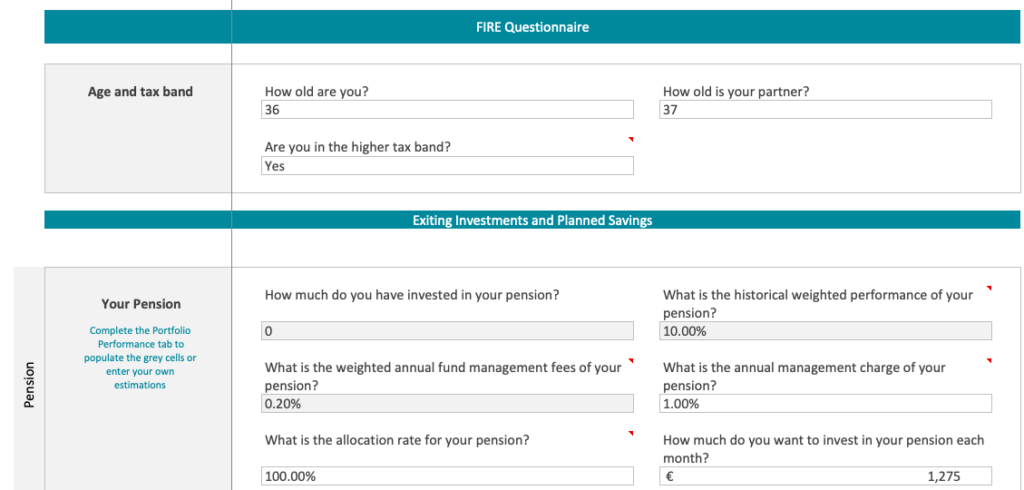

Couple decides to max pension contributions and saves 15,034€/year towards financial independence

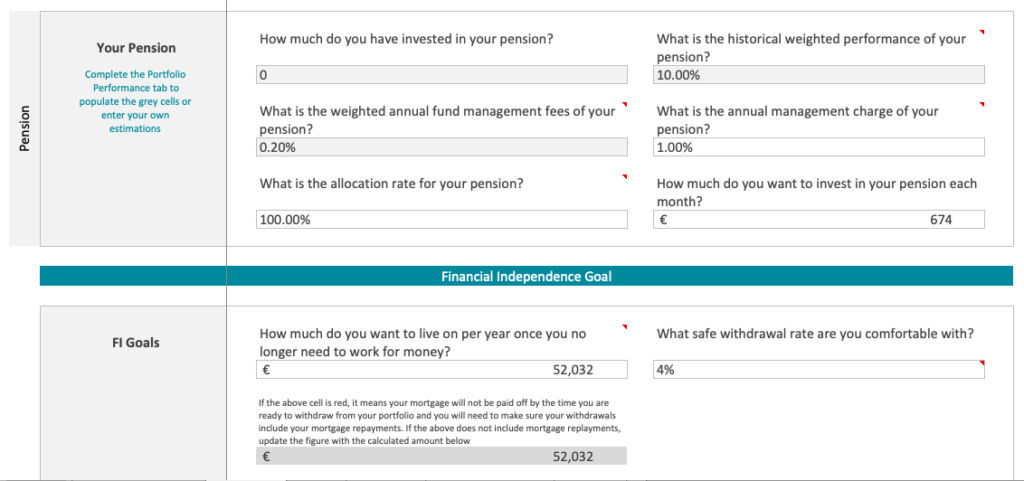

- Pension details:

- 100% allocation rate

- 1% annual management fee

- 0.20% annual fund mgmt fee

- 10% annual growth

- 1.9% inflation

- Note that to get this kind of pension performance and fees is not typical, it would require a very hands-on approach to ensuring the underlying funds are high performing and that the fees are low and the allocation rate is high. Not included are any commissions, bid/spread offers or monthly administrative charges which can also be charged.

Rent assumptions:

- An average rental price of 2,166€/month (or 25,992€/year) – the average between North and South Dublin prices as per Daft’s latest rental trend report.

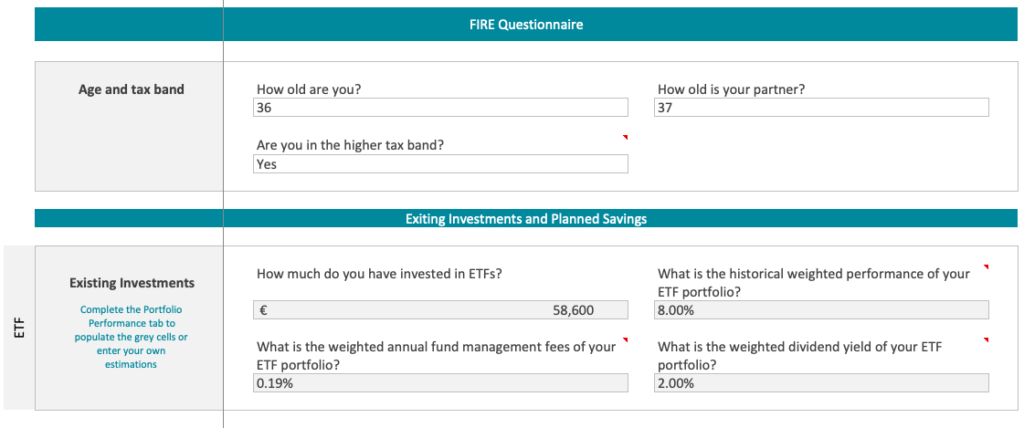

- Invest the money they would have put to a downpayment into an ETF portfolio: 58,600€

- ETF portfolio earns 8% per year and 2% in dividends which are reinvested, 0.19% management fees, and 1.9% inflation

- To maximise their savings the couple decide to invest the rest in a pension with the same performance and fees as the “buy” scenario

Total annual expenses: 62,832€

Total annual savings: 5,777€ post-tax or 8,087€ pre-tax in a pension

Time to Financial Independence: Buy

Using my FIRE calculator (which you can access on my paid member’s area), let’s see how the buy scenario plays out.

As they will not be overpaying their mortgage and maximising their pension instead, the annual expenses they will require to be fully financially independent will need to include their mortgage costs as they reach FI before their mortgage is paid off. They will no longer have childcare as their kids will be grown.

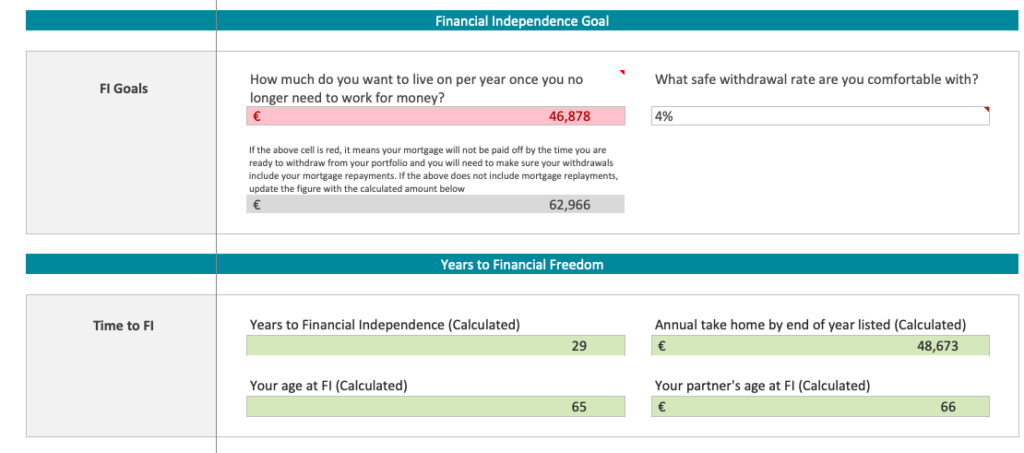

Annual expenses for FI: 57,678€ minus childcare 10,800€ = 46,878€

Time to FI if buying and investing: 29 years

So this option will take the couple 29 years to reach financial independence. 7 years after that their mortgage will be paid and they’re portfolio will be larger than they require, so they can reduce their withdrawal rate which will even further increase the chances of their portfolio not running out. This option leaves them with a higher net worth in the long run which could result in a better estate for their kids.

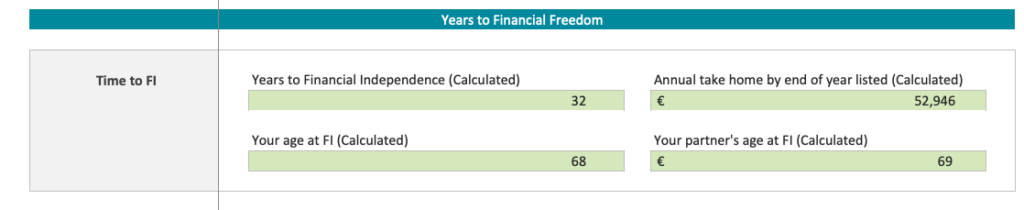

Time to Financial Independence: Rent

Again using the calculator, let’s see how this scenario plays out.

Keeping in mind their annual living expenses once financially independent will no longer include childcare so their 62,832€/year will go down to 52,032€/year.

Time to FI if renting and investing: 32 years

So renting and investing compared to buying and investing with these assumptions only makes a difference of 3 years.

Considerations

Neither scenario looks at the option of renting out a room in their home for additional income/savings to put towards investments. If they didn’t have kids or even once their kids are moved out they may want to bring on a lodger then OR even downsize and reduce their time to FI even further.

Once they get closer to FI and no longer need to work for money, they could decide to sell their home or rent/buy elsewhere in the country for cheaper and reach FI sooner.

Another option I didn’t look at in the buy scenario is to pay off the remainder of their mortgage with the tax free lump sum from their pension once they reach the access age, which MAY speed up their time to FI as their annual expenses would be reduced at that time.

I did not take into account any capital growth of the property as that is hard to estimate over a 30-year term and could go either way, though generally over that time frame it would go up potentially giving the opportunity to sell at a higher price and use that money to buy elsewhere in the country for cheaper and either reinvest the gains or buy a holiday home if that’s what they wished.

All this to say that if you want to become financially independent and are committed to investing, it doesn’t really matter if you rent or buy. Even in Dublin at current average rental and house prices.

If you work at fine-tuning your expenses to keep them low while not impacting happiness and investing what you can, when you can, you will reach your goal.

Keeping expenses low in the context of buying a house also means not buying a house outside of your means which is another post entirely but you can check out some of my own house buying tips here.

If you want to weigh up your own scenario’s with your own figures, my FIRE calculator is a great tool for comparing various options on your own path to financial independence. I’m always open to feedback and try to incorporate updates once a month to keep providing value.

Great article. Thanks for this. Did you include the 30,000 from HTB in that 58,600 eur to be invested if renting? Will the 30,000 make a difference in the final outcome ? Thanks.

Hi Guru, Thanks for the note. No, I did not include the first time buyer grant as I believe that only applies to new builds which will inevitably cost much more than the 400k example I gave. A quick search for new builds on Daft in Dublin city shows lowest price of 850k.